Scale Your CPA Firm Without Adding Headcount

Build your offshore team that works your way, trained, compliant, and white-labeled under your firm.

???? Book a Discovery CallTable of Contents

- Scale Your CPA Firm Without Adding Headcount

- Hundreds of Firms Have Already Used This Framework.

- Key Takeaways

- What Schedule P Actually Covers

- A Quick Word on Delivery

- Who Must Complete Schedule P

- Improve Margins Without Compromising Quality

- GILTI vs Subpart F on Schedule P

- What Schedule P Must Tie To

- Data You Need Before You Start

- Step‑by‑Step, Completing Schedule P

- Currency Rules Without the Headache

- Common Errors and How to Avoid Them

- When Schedule P Is Not Required

- Filing Deadlines, Extensions, and Penalties

- Related Schedules That Must Agree

- FAQs

- Final Checklist You Can Paste Into Your SOP

- Simplify Delivery, Improve Margins, Stay in Control.

Once your team tracks PTEP by annual accounts and groups, ties to Schedule J, and applies one translation policy, your reviews move faster and your downstream distributions stop tripping alarms.

Schedule P is your guardrail against double taxation. Get it right once, and downstream distributions stop creating surprises.

I wrote this guide to help you file it correctly, reduce back‑and‑forth with reviewers, and avoid penalties. Where it matters, I reference the latest IRS instructions and recent PTEP guidance, including how GILTI fits into PTEP, the role of functional currency, and what lines on Schedule P actually do.

Hundreds of Firms Have Already Used This Framework.

Join the growing list of CPA and accounting firms using Accountably’s Offshore Playbook to scale faster.

???? Get Your FREE Playbook

???? Visit Jugal Thacker’s LinkedIn

Send him a connection request and message “Playbook” to get your copy.

Key Takeaways

- Schedule P reports each U.S. shareholder’s Previously Taxed Earnings and Profits, in two parts, functional currency in Part I and U.S. dollar basis in Part II, and it must tie to Schedule J and your return.

- GILTI inclusions do create PTEP for section 959 purposes, and the IRS instructions show exactly where those amounts appear on Schedule P, for example line 7, column h.

- You maintain annual PTEP accounts and track PTEP groups, including groups attributable to Subpart F, section 965, and section 951A. The 2019 IRS notice and later guidance outline the grouping framework.

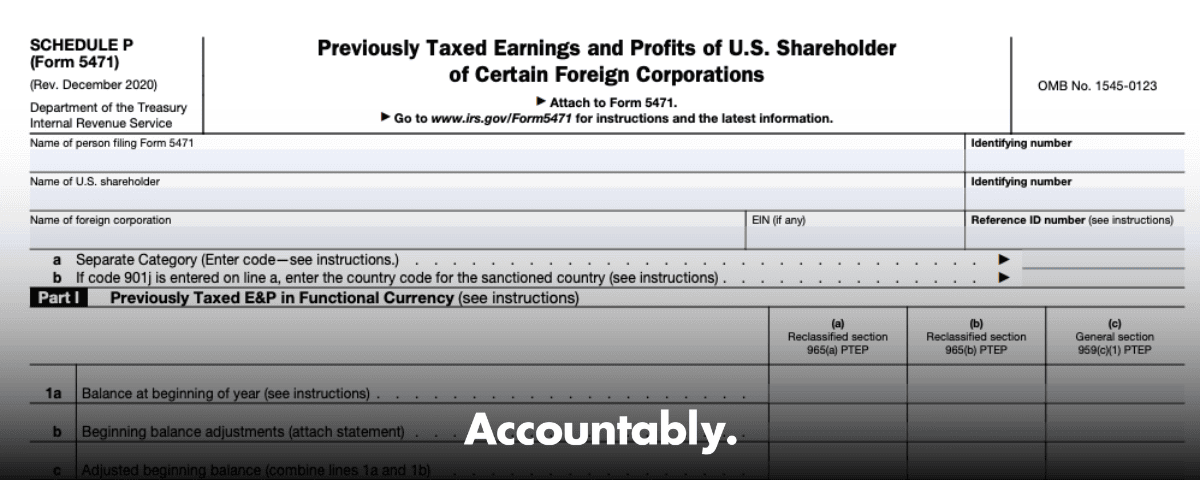

- Lines a and b at the top of Schedule P identify the separate category of income, and, if applicable, the 901j sanctioned country code. They are not opening balance or addition lines.

- Penalties are real. Failure to furnish 5471 information is generally $10,000 per annual accounting period per CFC, with additional $10,000 per 30 days after notice, capped at $50,000 extra.

What Schedule P Actually Covers

Schedule P captures your PTEP at the shareholder level, not just at the CFC level. Think of it as your personal ledger of amounts already taxed in the U.S., so later distributions can be excluded from income under section 959. The IRS instructions make two things clear, first, Part I is recorded in the CFC’s functional currency, and second, Part II converts that activity to your U.S. dollar basis for section 986(c) currency gain or loss tracking.

- Part I, functional currency, mirrors what sits inside Schedule J’s column e buckets when you wholly own the CFC, but will differ when multiple U.S. shareholders exist.

- Part II, U.S. dollars, sets the dollar basis in PTEP that you will use to compute currency gain or loss on distributions.

Why This Matters for Reviews

When Part I and Part II of Schedule P are clean, reviewers can quickly confirm three things, your annual PTEP accounts reconcile, GILTI and Subpart F inclusions were assigned to the correct groups, and distribution ordering matches section 959 and the IRS grouping approach described in post‑TCJA guidance. That is how you stop the five‑email chain on every dividend.

A Quick Word on Delivery

If your firm’s work slows at review, Schedule P is often in the pile. The pattern looks like this, unclear category codes, missing group assignments, and no single translation policy. In our work supporting U.S. CPA firms, we standardize PTEP logs, translation references, and tie‑outs to Schedules J, I‑1, and R to cut review time. If you handle this internally, the same structure applies. If you prefer a managed offshore model with disciplined SOPs and layered QC, a partner like Accountably can embed that structure without you giving up control. Use it only where it helps, keep the rest in‑house.

Who Must Complete Schedule P

You complete Schedule P if you are a Category 1a, 1b, 4, 5a, or 5b filer and you have PTEP with respect to the CFC. The instructions are explicit that each such filer must complete a separate Schedule P, including when relying on the joint filers exception for Form 5471 itself.

- Category 5 filers, U.S. shareholders of a CFC, complete Schedule P when PTEP exists.

- Category 1 filers related to section 965 specified foreign corporations remain on the hook while 965‑related E&P or PTEP persists.

Category 1b and 1c Nuances

The 1b and 1c subcategories exist for foreign‑controlled SFC situations and hinge on whether you are an unrelated section 958(a) U.S. shareholder or a related constructive U.S. shareholder. These rules were aligned with relief first described in Rev. Proc. 2019‑40 for similarly situated Category 5 filers. If this is your fact pattern, confirm attribution chains, related‑party status under section 954(d)(3), and whether Category 1 reporting is still required in a given year.

Improve Margins Without Compromising Quality

Offshore staffing helps firms deliver more, scale faster, and stay compliant, without adding local headcount.

???? Book a Discovery CallA Simple Filing Matrix

| Filer type | CFC or SFC status | PTEP present | Schedule P required |

| Category 5a or 5b U.S. shareholder | CFC | Yes | Yes |

| Category 1a, 1b, 1c | Section 965 SFC | 965‑related PTEP or E&P persists | Yes |

| Officer or director only, not a U.S. shareholder | Non‑CFC or no PTEP | No | Typically no |

| Constructive owner meeting an exception | As described in instructions | N/A | Often no |

Always test exceptions in the instructions for your category before you skip. The definitions and exceptions are detailed and highly fact specific.

GILTI vs Subpart F on Schedule P

Here is the point that trips many teams, GILTI does create PTEP for section 959 purposes. The Form 5471 instructions include an explicit example, where a shareholder reports section 951A PTEP on Schedule P line 7, column h, and Schedule J reflects aggregate section 951A PTEP at the CFC level. When multiple U.S. shareholders exist, each Schedule P carries only that shareholder’s PTEP, and Schedule J may be finalized in the following year to pick up the second shareholder’s amounts.

Post‑TCJA guidance also requires you to maintain annual PTEP accounts and segregate PTEP groups, including groups for section 951A, section 965, and Subpart F. This grouping affects distribution ordering, deemed paid taxes under section 960, and currency rules under section 986(c).

Why Your Prior Draft Might Say “GILTI is not PTEP”

Some older checklists blurred the distinction between GILTI mechanics and PTEP treatment. The current instructions and guidance close that gap. If your internal SOP still says “GILTI generally does not create PTEP,” update it and add the line‑level references so preparers stop second‑guessing reviewers.

What Schedule P Must Tie To

Schedule P does not live alone. Your tie‑outs should show:

- Schedule J, functional currency E&P and PTEP buckets for the CFC, with column mapping to Schedule P columns a through j.

- Schedule I and I‑1, current year Subpart F and GILTI data.

- Schedule R, actual distributions and their classification outcomes.

- Schedule E and E‑1 plus Forms 1116 or 1118, foreign taxes related to PTEP and their baskets.

Create a one‑page index in your workpapers that lists where each tie‑out lives. Your reviewer will thank you.

Data You Need Before You Start

You cannot build a clean Schedule P without a clean source set. Lock these down first.

- Opening and closing PTEP balances by annual account and group, with sources and dates.

- Current year additions and reductions, with Code cites, and the exchange rates used when relevant.

- Ownership details, including direct, indirect, and constructive paths under section 958, plus last‑day and maximum percentages.

- Prior E&P records and prior year Schedule P and Schedule J entries, so you can reconcile continuity.

This is the point where many teams stall. Build a short “PTEP data log” template and reuse it across CFCs.

Ownership Mapping That Actually Works

List each U.S. shareholder and the path of ownership to the CFC. Label which links are section 958(a) direct or indirect, and which are section 958(b) constructive. Capture related‑party status under section 954(d)(3) for Category 1b or 1c questions. Keep dated evidence in the file, stock ledgers, cap tables, and agreements that support changes during the year. The instructions rely on these definitions for category tests and exceptions.

Prior E&P and PTEP Records

Pull E&P from the first potential PTEP year forward, identify functional currency, and note your translation method. Tag each PTEP‑creating event, Subpart F, section 951A, section 965(a) and 965(b), and distributions. Then reconcile to your annual accounts so beginning, additions, reductions, and ending agree to the penny, and the currency policy is consistent with your Form 5471 as a whole.

Step‑by‑Step, Completing Schedule P

- Let’s translate the instructions into a workflow your staff can follow.

- Header and category lines a and b

- On line a at the top, enter the separate category of income code. If you are in a 901j sanctioned country context, line b carries the two‑letter country code. These are identification items, not balances.

- Part I, functional currency

- Enter the PTEP amounts in the CFC’s functional currency, consistent with Item 1h on page 1 of Form 5471. If you have pre‑1987 U.S. dollar PTEP, translate it into functional currency under Notice 88‑70 and add it to the right group.

- Part II, U.S. dollars

- Enter the U.S. dollar basis in PTEP. In general, this equals the U.S. dollar amount you included in income, and you will use it for section 986(c) currency gain or loss calculations.

- Line 1b difference adjustment

- If last year’s ending balance does not equal the amount that should have been the ending balance after modifications, use line 1b in Schedule P to reconcile and attach an explanation.

- Column mapping and tie‑outs

- Columns a through j on Schedule P correspond to Schedule J, Part I, column e sub‑buckets. Use the IRS mapping so reviewers can check across schedules quickly.

Pro tip, place your tie‑out references in a margin note on the PDF you route for review. It cuts questions in half.

Currency Rules Without the Headache

Two rules keep you out of trouble. Part I is functional currency. Part II is U.S. dollars. Apply one translation policy everywhere else on Form 5471 and document it once.

- Functional currency, determine it and keep a memo on why, typically the currency of the primary economic environment. Report functional currency amounts on Schedule P, Part I, and translate only where the schedule requires U.S. dollars.

- U.S. dollar translation, for balance items use appropriate year‑end rates, for flow items use average or transaction‑date rates depending on the rule being applied, and follow the “divide‑by convention” the IRS calls out in the 5471 instructions.

- DASTM, if the CFC uses DASTM, follow Reg. §1.985‑3, then carry those amounts into your 5471 schedules per the special instructions, and disclose when required.

Annual PTEP Accounts and Groups

Post‑TCJA, you maintain annual accounts and segregate PTEP into groups, for example section 951A PTEP, section 965(a) PTEP, and others. The 2019 IRS notice lays out the grouping framework, and subsequent guidance refines ordering and basis interaction. Know the groups you actually have, and do not create buckets that never arise in your facts.

Distribution Ordering

Ordering matters, especially when you still have section 965 PTEP in the stack. The notice framework prioritizes section 965(a) and 965(b) PTEP before applying a last‑in, first‑out approach for remaining section 959(c)(2) PTEP groups, then moves to section 959(c)(3) E&P. If you are still distributing 965 PTEP, say so in your workpapers and show the math.

Common Errors and How to Avoid Them

- Treating GILTI as “not PTEP.” Update your SOPs and use the line‑level example in the 5471 instructions to guide staff.

- Mixing currencies within Part I. Part I is functional currency, full stop. Part II is where dollars live for PTEP basis and section 986(c).

- Missing line 1b reconciliation. If last year’s ending and this year’s beginning do not match, fix it on line 1b and attach an explanation.

- No tie to Schedule J. Use the columns mapping in the instructions and show the relationship in your workpapers so reviewers can cross‑check quickly.

- Inconsistent exchange rate conventions. The instructions require a divide‑by convention. Document rates and keep a one‑page exchange rate schedule in your file.

If you are fixing last year’s translation approach, document why, show the recalculation, and explain the tax effect so the story is clear on review.

When Schedule P Is Not Required

You can usually skip Schedule P when there is no PTEP with respect to the CFC for the year, and your filer category does not otherwise require it. Common cases:

- You are filing Form 5471 for an officer or director role with no U.S. shareholder status and no PTEP.

- You are a constructive owner who meets a listed exception in the instructions.

- The foreign corporation is not a CFC and no PTEP exists.

Always confirm no PTEP exists from prior inclusions, section 965, section 951A, or Subpart F, and that no qualifying distribution occurred during the year. If in doubt, check the category exceptions section of the instructions relevant to you.

Quick Self‑Audit Before You Omit

- Any Subpart F or section 951A inclusion ever? Any 965 inclusion or reclassification? If yes, you probably have PTEP.

- Any distribution this year from the CFC? Check ordering and see if it touched PTEP.

- Any ownership changes that could reclassify balances?

If you can document “no” across that list and your category exceptions apply, omit Schedule P and note “no PTEP” in your file.

Filing Deadlines, Extensions, and Penalties

Schedule P rides with Form 5471, which rides with your income tax return. The due date matches your return’s due date, and valid extensions cover Schedule P. If you file late or incomplete, penalties apply under section 6038 and 6046, generally $10,000 per annual accounting period per foreign corporation, plus $10,000 per 30 days after notice if the failure continues, capped at $50,000 additional. Put a calendar reminder at least 30 days before the extension deadline.

Amending a Filed Schedule P

If you find an error, file an amended Form 5471 with an amended income tax return. Check the “Amended” box, include the corrected Schedule P, and attach an explanation that shows what changed and why. If tax changes flow through, include those forms and pay tax, interest, and any penalties due. Keep a clean record to respond quickly to notices.

Related Schedules That Must Agree

- Schedule J, the CFC‑level E&P and PTEP, in functional currency, with column e buckets that correspond to Schedule P’s columns.

- Schedule I and I‑1, Subpart F and GILTI details used by U.S. shareholders and Form 8992.

- Schedule E and E‑1, cumulative taxes and PTEP‑related taxes by basket, with the divide‑by convention.

- Schedule R, distributions and classification outcomes under section 959.

Tip, put a short distribution ordering memo in the file whenever you touch section 965 PTEP or have multiple PTEP groups. Your future self will be grateful.

FAQs

What is Schedule P of Form 5471 used for?

It is where each U.S. shareholder tracks their PTEP by annual account and group, in functional currency in Part I and U.S. dollars in Part II, so later distributions can be excluded from income under section 959 and currency gain or loss can be computed under section 986(c). It must reconcile to Schedule J and other schedules.

Does GILTI create PTEP?

Yes. Section 951A inclusions create PTEP for section 959 purposes, and the IRS instructions show how to report those amounts on Schedule P, for example line 7, column h, with a coordinating example.

How do I handle functional currency versus U.S. dollars?

Use functional currency in Part I and the U.S. dollar basis in Part II. Apply a consistent translation approach elsewhere on Form 5471 and use the IRS divide‑by convention when you must show exchange rates.

What are the current penalties if I miss Schedule P?

For failure to furnish required information, the penalty is generally $10,000 per foreign corporation per annual accounting period, plus $10,000 per 30 days after IRS notice if the failure continues, up to $50,000 more.

Are there new rules on PTEP groups I should know?

The IRS described annual accounts and multiple PTEP groups in Notice 2019‑01, expanded in later guidance. Proposed regulations released November 29, 2024, address PTEP accounting and basis adjustments. Treat them as proposed until finalized, and follow the instructions in force for your filing year.

Final Checklist You Can Paste Into Your SOP

- Confirm filer category and exceptions.

- Build the PTEP data log, beginning balances, inclusions, distributions, groups, and rates.

- Map ownership with section 958(a) and 958(b) paths and related‑party status.

- Complete Schedule P, line a category code, line b if 901j applies, Part I functional currency, Part II U.S. dollar basis, and line 1b differences with an attachment.

- Tie to Schedule J, I‑1, E/E‑1, and R with a one‑page index.

- Review exchange rate disclosures using the divide‑by convention.

- Calendar the return due date and extension, then run a pre‑file penalty check.

Simplify Delivery, Improve Margins, Stay in Control.

Offshore support that works exactly like your in-house team.

???? Let’s Talk