Scale Your CPA Firm Without Adding Headcount

Build your offshore team that works your way, trained, compliant, and white-labeled under your firm.

👉 Book a Discovery Call

If you have ever felt growth stall because your team is buried in production and review loops, this guide will help you regain control. Form 14711-A is a simple worksheet with a big job. You use it to forecast the stream of future 8038‑CP refund claims tied to a bond issue, so your case plan, review time, and statute protection steps are never a scramble. It complements, not replaces, the statute evaluation work you document elsewhere.

Accountably note, brief and only where useful, if your firm needs disciplined offshore help to standardize 8038‑CP workpapers and keep future‑return forecasting on schedule, our U.S.‑led teams can plug into your workflow without adding chaos. More on that later, if it is relevant to your operation.

Key takeaways

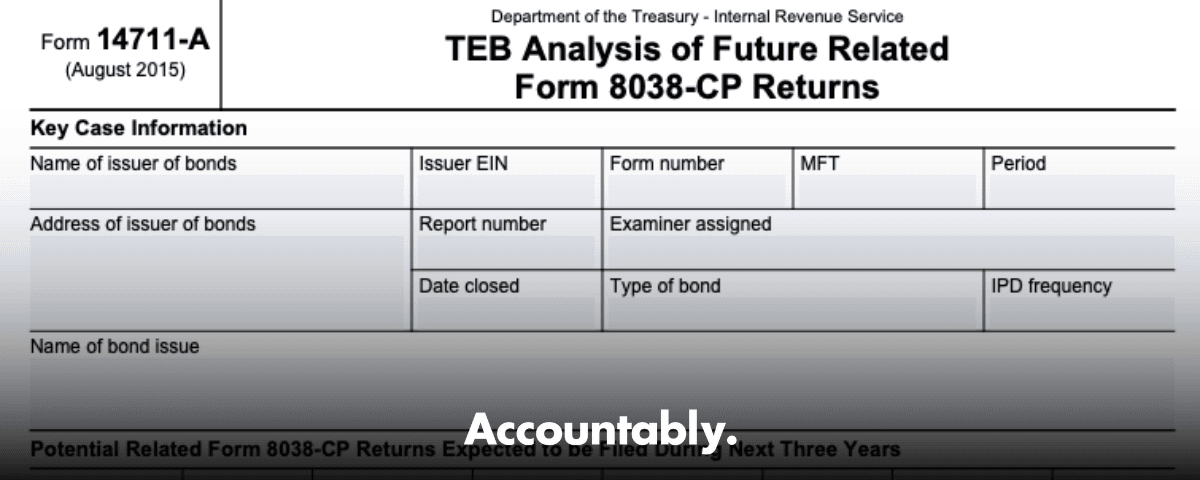

- Form 14711‑A is the “look‑ahead” worksheet, TEB Analysis of Future Related Form 8038‑CP Returns. You use it to list the 8038‑CP claims you expect over the next three years for the bond issue under exam. It is a planning tool, not a statute control form. (irs.gov)

- Form 14711‑B is where you evaluate and control statutes for related 8038‑CP returns. IRS procedures require pulling the Debt Service Schedule, getting the DPBCRC list of filed or expected 8038‑CP returns, and updating the statute evaluation at least every six months. Use 14711‑A to anticipate volume, then 14711‑B to protect the clock. (irs.gov)

- Direct Pay Bond claims, for BABs, RZEDBs, QZABs, QSCBs, NCREBs and QECBs, still run through Form 8038‑CP. Instructions were last reviewed in January 2025 and include e‑file notes and attachment rules. (irs.gov)

- Refund payments processed on or after October 1, 2020 through at least September 30, 2031 are reduced by a 5.7% sequestration rate. Plan your 14711‑A expectations with that reduction in mind. (irs.gov)

- Treat 14711‑A as part of your delivery system. When you forecast future filings, you prevent review bottlenecks, prioritize consent‑needed cases, and avoid last‑minute paper chases for payee data or ACH details. TE/GE’s TEB program guidance frames the mission and process for these exams. (irs.gov)

What Form 14711‑A actually is

Form 14711‑A is a one‑page planning worksheet issued by the IRS for Tax‑Exempt Bonds. The title says exactly what it does, TEB Analysis of Future Related Form 8038‑CP Returns. In practice, you list each period in the coming three years when a related 8038‑CP claim is likely and estimate the credit amount. This gives your team a realistic runway to schedule reviews, request consents when needed, and set workload expectations with managers. (irs.gov)

Hundreds of Firms Have Already Used This Framework.

Join the growing list of CPA and accounting firms using Accountably’s Offshore Playbook to scale faster.

💬 Get Your FREE Playbook

👉 Visit Jugal Thacker’s LinkedIn

Send him a connection request and message “Playbook” to get your copy.

Think of 14711‑A as your flight plan. You are not flying yet, you are charting the route so there are no surprises mid‑air.

Where teams get tripped up is mixing 14711‑A and 14711‑B. 14711‑A forecasts. 14711‑B controls statutes. The Internal Revenue Manual tells examiners to request the DPB Compliance Database list and the current Debt Service Schedule, then prepare and keep 14711‑B current, updating at least every six months. Use both forms together and your case feels calm instead of reactive. (irs.gov)

Why this matters for your delivery and growth

If you run a CPA, EA, or municipal finance practice, your problem is rarely a lack of demand. The ceiling is delivery, especially during peak season or when multiple DPB cases hit at once. Without a forward view of 8038‑CP filings, partners end up trapped in review loops, statute dates creep up, and quality wobbles under time pressure. I have seen great teams lose days chasing a missing payee EIN or a delayed DSS while a consent deadline ticked down. That is avoidable.

Improve Margins Without Compromising Quality

Offshore staffing helps firms deliver more, scale faster, and stay compliant, without adding local headcount.

👉 Book a Discovery CallForm 14711‑A restores predictability. When you chart the next twelve to thirty‑six months of claims tied to a bond, you can:

- Block review time before calendars fill up.

- Sequence consent requests for returns with less than a year on the clock, using 14711‑B to document the plan.

- Coordinate communication, so payee details and ACH info are confirmed before submission windows open.

- Model post‑sequestration cash expectations, which helps issuers and designated payees manage their budgets. (irs.gov)

Programs covered and current context

Direct Pay Bonds with refundable credits continue to use Form 8038‑CP for claim processing. The IRS instructions, last reviewed on January 14, 2025, cover BABs and the specified tax credit bonds that were eligible for direct pay elections, including RZEDBs, QZABs, QSCBs, NCREBs, and QECBs. If you are setting up 14711‑A today, use those instructions to make sure your attachment set and data formatting match current IRS expectations, including e‑file compatibility and Schedule A rules. (irs.gov)

A practical note, sequestration applies to refund payments processed in fiscal years 2021 through 2031 at a 5.7% reduction. Your 14711‑A credit estimates should reflect this reduction so stakeholders are not surprised by the net received. Build the rate into your planning and reference the IRS sequestration notice in your workpapers. (irs.gov)

14711‑A vs. 14711‑B, how they work together

- 14711‑A, plan the next three years of related 8038‑CP filings and expected credit amounts. It is a forecasting sheet that keeps your team ahead of volume and timing. (irs.gov)

- 14711‑B, evaluate and control statutes for the related returns you identified. The IRM instructs examiners to request the DSS and the DPBCRC Excel list, then prepare 14711‑B and update it at least every six months. Use RCCMS statute tools or Form 895 where required, and secure managerial approval before establishing related case controls. (irs.gov)

When you pair the two, 14711‑A sets the calendar and 14711‑B protects the calendar. That is the simplest way to keep delivery tight and reviews sane.

How to complete Form 14711‑A with confidence

Use this as your repeatable playbook. It keeps the work clean and your reviewers fast.

Gather the right inputs first

- Issuer identifiers, issuer EIN, issue date, issue price, IRS report number.

- Core schedules, the current Debt Service Schedule that shows principal and interest by payment date.

- DPB data, the most recent DPB Compliance Database extract that lists related or expected Form 8038‑CP returns, including payee EINs, claim dates, claimed amounts, and filing dates.

- Crosswalk, a simple index that ties each DSS payment date to a related or expected 8038‑CP claim.

Quick tip: Align file names and tabs so reviewers can jump between DSS, payee list, and the 14711‑A without hunting. Two clicks, not ten.

Fill out the worksheet

- Identify each upcoming interest payment date over the next three years.

- For each date, record the expected related 8038‑CP claim, the payee EIN, and the estimated refundable credit amount.

- Note any changes in designated payee status so you are not surprised by a different EIN on the filed return.

- Add a comment whenever you expect an amended claim, a reassignment, or a filing delay.

Keep paragraphs short and entries precise. Your goal is to make reviews fast and predictable.

Keep reviews friction‑free

- Use structured workpapers, standardized naming, and version control.

- Add an “internal completeness check” checklist, file present, dates validated, payee EIN matched, totals tied to DSS, sequestration noted.

- Save a PDF snapshot of each 14711‑A version and keep your editable workbook in the live folder so history and current state are both clear.

Submission timing and updates

Prepare Form 14711‑A when you open the Direct Pay Bonds examination. Then set calendar reminders to refresh the worksheet at least every six months. Accelerate that schedule if you see amended filings, correspondence that affects timing, or changes in payee information.

Bottom line, prepare on day one, then update every six months, faster if something material changes.

A practical cadence that works:

- Week 1, request the DSS and the DPB extract via secure email, include issuer EIN, issue date, issue price, and report number.

- Week 2, populate 14711‑A, tie it to DSS and the extract, and get a quick manager review.

- Ongoing, when you issue a Form 5701‑B or reach an adverse determination, update 14711‑A the same week and note any new related cases you need to open.

- Six‑month cycle, refresh DSS, pull a current extract, and re‑run your completeness checks.

Required approvals and signatures

Use your approval authority matrix so the right people sign at the right time. Routine planning and updates usually sit with the examiner and Group Manager. Escalate if your forecast implies multiple related 8038‑CP exams, sensitive procedures, or program‑level impacts. In those cases, get Program Manager or Director sign‑off and keep the signed page with the permanent file.

Acceptable signature methods

- Original signatures or secure electronic signatures are fine if you document the contact and store the transmission log.

- Faxed or scanned signatures are acceptable once you have documented the taxpayer contact and followed internal signature rules.

- Re‑approve whenever your evaluation changes, at least every six months, and keep name, title, and date clear on each version.

Documentation to include with your request

When you circulate or submit the worksheet, include the materials reviewers need to validate every entry without guesswork.

Include issuer EIN, bond details, IRS report number, and aligned attachments so everything ties out cleanly.

- Debt Service Schedule, complete, with payment dates and amounts. Flag dates that have related or expected 8038‑CP claims.

- DPB extract or Excel list, show payee EINs, claim dates, claimed amounts, and filing dates.

- Relevant correspondence, for example Form 5701‑B, no‑consideration letters, and amended filings.

- Cross‑references, show where each item appears in your folder structure and in the 14711‑A comments.

Processing timeline and notifications

Before you open the case file fully, build your timeline using Form 14711‑A so you know when claims are likely to hit and how that maps to review capacity. Then create simple notification triggers.

- Trigger 1, when you issue a Form 5701‑B, update 14711‑A within the week and list any affected related returns.

- Trigger 2, when an adverse determination is made, mirror that change in 14711‑A, identify related exams to open, and plan statute protection steps using your statute tools and statute worksheet.

- Trigger 3, set a 90‑day look‑ahead reminder for upcoming claim dates so you can confirm payee EINs and supporting schedules.

Simple workflow table

| Step | Owner | What you do | Proof of completion |

| Request DSS and DPB extract | Examiner | Send secure email with issuer EIN, issue date, issue price, report number | Email and receipt log |

| Build 14711‑A draft | Examiner | Populate three‑year forecast, link to DSS and extract | Saved workbook and PDF snapshot |

| Quick review | Group Manager | Spot check ties and comments | GM initials and date |

| Notifications set | Examiner | Calendar 90‑day and 6‑month reminders | Calendar entries |

| Six‑month refresh | Examiner | Pull current DSS and extract, re‑validate | Updated 14711‑A and checklist |

| Escalation, if needed | Program Manager or Director | Approve sensitive or multi‑case actions | Signed page, name, title, date |

Accountably note, optional, if you want help standardizing this workflow, our teams can operate inside your systems, QuickBooks, Thomson Reuters, CCH, Karbon, TaxDome, and maintain the same naming, checklist, and review logic so nothing slips during peak season. We keep references light because the focus is your process, not our promo.

Continuous registration considerations

Form 14711‑A is a planning sheet, yet it plays a big role in keeping your registration trail continuous and auditable. Treat it as the anchor that ties issuer identifiers, the DSS, the payee EIN list, and every related filing together throughout the life of the examination.

- Validate DSS to payee alignment. Reconcile scheduled interest payments with identified payees and expected or filed 8038‑CP returns.

- Refresh when facts change. If a payee is reassigned, a payee EIN changes, or the DSS is updated, revise 14711‑A the same week.

- Preserve permanency. Keep the latest version and a snapshot history in the permanent file so your decisions are easy to follow later.

Impact on registration and enrollment status

Use the worksheet to spot eligibility changes early. If an issuer switches to a designated payee, if an adverse bond qualification finding affects claim rights, or if duplicate claims appear, update 14711‑A immediately and document the who, the when, and the why.

Eligibility changes to capture

- Record the change, issuer EIN versus designated payee EIN, and the effective payment periods.

- Identify related 8038‑CP returns with at least 180 days remaining and plan consent or protection steps if needed.

- Reflect any adverse determinations, duplicate filings, or amended claims and attach the supporting correspondence.

Common mistakes to avoid

- Missing the Debt Service Schedule. Without the DSS, payment dates and amounts are guesswork. Always attach it.

- Incomplete DPB requests. If your secure email does not include issuer EIN, issue date, issue price, and report number, you will not get a clean list back.

- Stale updates. If you do not update at least every six months, you lose the thread when filings change or payees shift.

- Payee mismatches. Verify whether the return is under the issuer EIN or a designated payee EIN so your forecast matches reality.

Simple rule, if it affects who files, when they file, or how much they claim, it belongs in the 14711‑A update and the attachments.

Contact information and support

Keep contacts visible on the first tab of your workbook, not buried in email chains. Record secure email addresses, phone numbers, and escalation paths for your DPBCRC contact, TEB technical contact, your Group Manager, and any coordinator.

| Role | Primary method | Escalation path |

| DPBCRC | Secure email | Manager, Program Lead |

| TEB Technical | Secure email | Technical Advisor |

| Examiner | Secure email or phone | Group Manager |

| Coordinator | Secure email | Territory Manager |

Follow your secure transmission instructions whenever you share issuer EINs, issue dates, issue prices, and report numbers. Save the latest version of 14711‑A in the permanent file so anyone stepping into the case can orient in minutes.

FAQs

Why did I receive a Form 14611?

You received Form 14611 for identity verification tied to a recent tax matter. Read the letter carefully and respond by the stated date so processing does not stall. If the address is wrong, follow the instructions to correct it and keep a copy in your file.

What is a RAIVS request?

RAIVS is a records request from the IRS. It specifies which documents and time periods you need to send, and it comes with a deadline. Provide exactly what they ask for in the format they request and save proof of transmission for your case file.

What is Form 8611?

Form 8611 is used to calculate the recapture of low income housing credits when a project fails to meet ongoing requirements. If it applies to your engagement, confirm periods, compute the additional tax, and note that there is no automatic penalty relief. Keep the computation workpapers with your return support.

Conclusion and next steps

You now have a practical way to make Form 14711‑A work for you, not against your calendar. Set it up on day one, tie it tightly to the DSS and your DPB extract, and refresh it at least every six months. Use it to schedule reviews, anticipate payee changes, and keep related 8038‑CP filings from becoming fire drills.

Treat planning as a deliverable. When you plan well, reviews are shorter, deadlines are met, and clients trust your process.

If your team is stretched thin during peak cycles and you want help standardizing workpapers, reviews, and updates inside your own systems, Accountably can provide trained offshore teams that plug into your templates and tools, maintain your naming and review logic, and keep the updates on schedule. No resume farming, just disciplined execution that reduces review time and revision cycles.

Simplify Delivery, Improve Margins, Stay in Control.

Offshore support that works exactly like your in-house team.

💼 Let’s Talk