Scale Your CPA Firm Without Adding Headcount

Build your offshore team that works your way, trained, compliant, and white-labeled under your firm.

???? Book a Discovery CallTable of Contents

- Scale Your CPA Firm Without Adding Headcount

- Key Takeaways

- What Form 56-F Is, And Who Actually Files It

- Hundreds of Firms Have Already Used This Framework.

- When To File, The 10‑Day Clock And Annual Refresher

- Where To File, Two Tracks You Need To Know

- What To Include, A Short Checklist

- Improve Margins Without Compromising Quality

- How To Complete Form 56-F Correctly

- Form 56 vs. Form 56‑F, Clear Differences

- Common Filing Mistakes And How To Avoid Them

- A Simple, Repeatable 56‑F Workflow

- Security, Recordkeeping, And Audit Readiness

- Where Accountably Fits, Only If You Need Hands‑On Help

- FAQs About IRS Form 56‑F

- Tools, Templates, And A Clean Filing Kit

- Compliance Notes And YMYL Care

- Wrap Up And Next Steps

- Simplify Delivery, Improve Margins, Stay in Control.

The team had done the right thing on tax returns, but they missed the notice that changes who the IRS should talk to. That notice is Form 56-F, and if you work with receiverships, conservatorships, or you advise on troubled bank situations, you cannot afford to get this wrong.

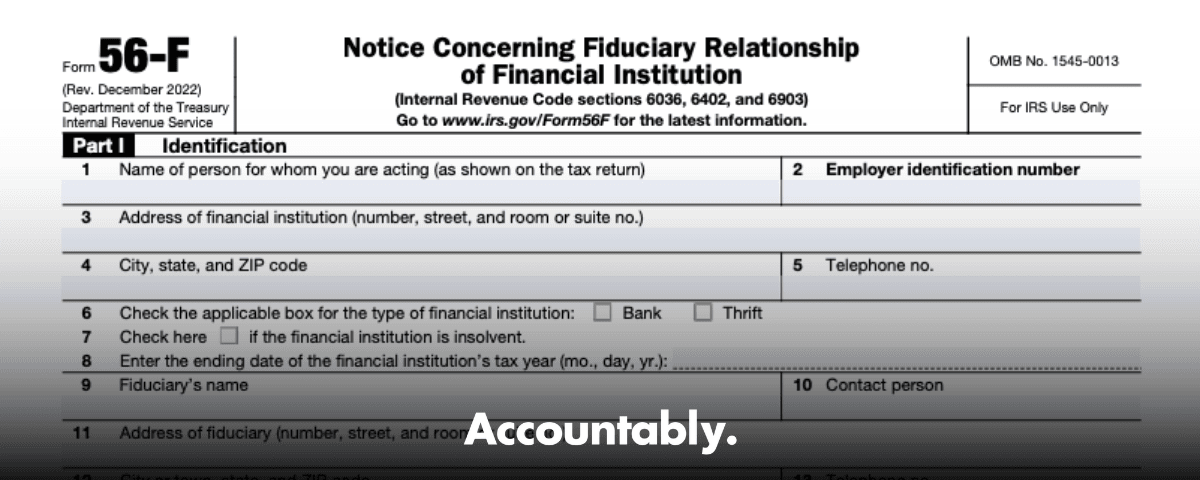

Form 56-F is the IRS notice that tells the Service who the fiduciary is for a financial institution, so IRS correspondence and refund rights go to the right place, at the right time.

Key Takeaways

- Form 56-F is for financial institutions, and the filer is typically a federal agency acting as receiver or conservator, for example the FDIC, not the bank’s ordinary accounting staff.

- File within 10 days of appointment, then again each year you continue in that role for refund purposes under section 6402, and file again when the fiduciary relationship ends.

- Where to file depends on purpose. For sections 6402 and 6903, send it to the IRS Service Center where the financial institution files its income tax return. For 6036, send it to the IRS Advisory Group Manager with jurisdiction.

- If the bank is or was in a consolidated group, special refund rules apply under the consolidated return regulations, updated December 30, 2024. Copy the common parent when required.

- The current PDF is Rev. December 2022 and remains the active revision as of June 24, 2025, on IRS.gov. Always pull the form from the IRS page before filing.

What Form 56-F Is, And Who Actually Files It

Form 56-F is the IRS notice for fiduciary relationships tied to a financial institution, such as a bank or thrift. The point is simple, you are telling the IRS who should receive notices and handle tax matters for that institution while it is in receivership or conservatorship. The form exists alongside Form 56, but it is not the same. Form 56-F is tailored to financial institutions and the unique refund and consolidated group rules that can come into play.

Here is the part many teams misunderstand. The party that files Form 56-F is the federal agency serving as the fiduciary, for example the Federal Deposit Insurance Corporation, or another federal entity authorized by law, not the bank’s internal staff. If you sit inside a bank and you are not the appointed receiver or conservator, Form 56-F is not your form. If you represent a decedent’s estate, a trust, or a company that is not a bank, that is Form 56, not 56-F.

Hundreds of Firms Have Already Used This Framework.

Join the growing list of CPA and accounting firms using Accountably’s Offshore Playbook to scale faster.

???? Get Your FREE Playbook

???? Visit Jugal Thacker’s LinkedIn

Send him a connection request and message “Playbook” to get your copy.

When To File, The 10‑Day Clock And Annual Refresher

Timing is tight. You must file within 10 days of the fiduciary’s appointment. If the fiduciary continues in that role, file again each subsequent tax year for refund purposes under section 6402, which protects your position on any refunds that relate to consolidated return years. If the institution later becomes insolvent after an initial filing for a solvent bank, file a new 56‑F and check the insolvency box on line 7. Finally, when the fiduciary relationship ends, file to terminate. These filings keep IRS records aligned with who has authority at each step.

Practical example, if the appointment is dated March 10, your 10‑day window runs to March 20. Do not wait for the first IRS letter to show up, file immediately and keep proof of mailing in the case file.

Where To File, Two Tracks You Need To Know

Your filing destination depends on why you are filing:

- For section 6402 refunds and section 6903 fiduciary notice, mail Form 56‑F to the IRS Service Center where the financial institution files its income tax return.

- For section 6036 receivers and similar fiduciaries, send Form 56‑F to the Advisory Group Manager for the area office with jurisdiction, as listed in Publication 4235.

The IRS also publishes a live “Where to file” page that confirms Form 56-F routing and notes when addresses change mid‑year. For 2026 use, verify the address there before you ship the packet.

What To Include, A Short Checklist

- Financial institution details and EIN, plus the tax year end date.

- Fiduciary name and contact, for example FDIC receiver, with a direct contact person.

- Evidence of authority, attach the court order or appointment, replacement, or order of insolvency.

- Consolidated group information, if applicable, and whether a copy was sent to the common parent.

- Scope of notices, specify other taxes or periods for correspondence beyond income, employment, or excise.

- Termination evidence, when ending the relationship, attach the court order or dissolution certificate.

Tip, always keep a clean packet copy, certified mail proof, and a transmission log in the workpapers. It saves hours if you ever need to prove the notice date.

Improve Margins Without Compromising Quality

Offshore staffing helps firms deliver more, scale faster, and stay compliant, without adding local headcount.

???? Book a Discovery CallHow To Complete Form 56-F Correctly

I like to prep 56‑F the same way I would prep a clean close file, start with authority, then identities, then routing. Here is a simple flow you can follow.

Step 1, Confirm Authority And Gather Exhibits

Pull the appointing order that names the receiver or conservator. If the institution is insolvent, note the statute cited in the order. You will check the insolvency box on line 7 and attach the order as the authority exhibit. This documentation is not just for the IRS, it is your audit trail inside the case file.

Step 2, Complete Identification For The Institution And The Fiduciary

Enter the financial institution’s legal name and EIN, address, and year end. Enter the fiduciary’s legal name, for example FDIC, and a live contact person who can speak to tax matters. If the institution is, or was, part of a consolidated group, complete lines 16 through 21. Check the box to confirm you sent a copy to the common parent when required.

Step 3, Declare The Scope Of IRS Notices

By default, income, employment, and excise notices for the institution will route to the fiduciary. If you want other notices routed as well, list the types and periods in Part III. This prevents important correspondence from landing with the wrong party during a sensitive period.

Step 4, Address Consolidated Group Rules

If the institution sits in a consolidated group, refunds can become complicated. Regulations under section 6402 let the IRS deal directly with the fiduciary for refunds that relate to the institution’s losses, even though consolidated return rules normally put the common parent in charge. Copy the common parent when required and keep evidence of that notice in your file. The regulation was updated on December 30, 2024, so make sure your internal playbook reflects the current text.

Step 5, File On Time And Keep Proof

File within 10 days of appointment, then file annually if you remain in place for refund purposes, and file again to terminate. Send it to the correct Service Center or to Advisory, depending on why you are filing, and keep certified mail receipts and a digital copy in your DMS.

Step 6, Sign And Title

Sign under penalties of perjury, and include the title that matches your role, for example Receiver or Conservator. Make sure the signer is the authorized official specified in the order.

Form 56 vs. Form 56‑F, Clear Differences

Use Form 56 for general fiduciary notices, for example estates, trusts, guardians, and non‑bank entities. Use Form 56‑F only for financial institutions where a federal agency is the fiduciary. If your work involves a decedent’s final Form 1040 or a trust’s Form 1041, that is Form 56. If your work involves an FDIC receivership of a bank, that is Form 56‑F.

Quick Comparison

| Item | Form 56 | Form 56-F |

| Who files | Executor, trustee, guardian, assignee, other fiduciaries | Federal agency acting as receiver or conservator of a financial institution |

| What it covers | Creation, change, or termination of fiduciary relationship under §§ 6903 and 6036 | Same core notice, plus consolidated refund mechanics for banks under § 6402 and related regs |

| Timing | File when you start, change, or end the role | File within 10 days of appointment, then annually if still acting for refund purposes, and on termination |

| Where to file | Service Center where the person files returns, plus Advisory in special cases | Service Center for §§ 6402 and 6903 filings, Advisory for § 6036 filings |

Sources, see IRS About Form 56, IRS About Form 56‑F, and the 56‑F PDF instructions.

Common Filing Mistakes And How To Avoid Them

You can do everything right on the tax side and still create weeks of cleanup if Form 56‑F is off by even a little. Here are the mistakes I see most often, plus simple fixes you can put in place today.

Treating 56‑F Like A One‑And‑Done

Teams file once at appointment, then forget the annual filing for refund purposes or the final termination notice. Set a reminder in your case timeline for the anniversary month, and add a closeout step for termination. Your future self will thank you.

Missing Consolidated Group Steps

If the financial institution was in a consolidated group, you may need to notify the common parent and keep proof in the file. Skipping this creates refund disputes that are avoidable. Add a checkbox in your intake to ask, was the bank part of a consolidated group, and if yes, who was the parent.

Incomplete Authority Attachments

The form lets you reference the appointing order, but the reviewer who picks up your file six months later will want the full text. Always attach the signed appointing order, any replacement orders, and any document that shows insolvency status. Keep a scanned, text‑searchable copy in your DMS.

Wrong Mailing Address

Where you file depends on purpose. Filing a section 6036 notice to the Service Center, or a section 6402 notice to Advisory, slows everything down. Build a short routing guide into your SOP so staff double check the destination before sealing envelopes.

No Proof Of Mailing

If a notice goes astray, proof of mailing saves the day. Use certified mail, log the tracking number in the workpapers, and save the USPS proof with the packet PDF. It is a small step that prevents big headaches.

If you cannot prove when the notice went out, plan on extra calls and delays. Make certified mailing and a clean PDF packet non‑negotiable.

A Simple, Repeatable 56‑F Workflow

You do not need a huge checklist. You need a tight sequence your team can run every time.

- Intake

- Confirm the bank’s legal name, EIN, and tax year end.

- Gather the appointing order, any replacement orders, and current contact info for the fiduciary official.

- Ask if the bank is part of a consolidated group, and record the common parent details if yes.

- Draft

- Complete identification for the bank and the fiduciary.

- Check the insolvency box if applicable, and reference the specific order.

- For consolidated group cases, complete the related section and note who was copied.

- Review

- Senior reviews the form against the source documents.

- Verify mailing address based on the purpose, section 6402 or 6903 to the Service Center, section 6036 to Advisory.

- Confirm the 10‑day clock and the planned mail date.

- File

- Print and sign with the correct title.

- Mail via certified mail, and scan the signed copy.

- Save the packet PDF, the tracking receipt, and a one‑page filing memo in the DMS.

- Maintain

- Add a tickler for the annual filing if still acting as fiduciary for refunds.

- When the relationship ends, run the termination filing with the same discipline.

Timeline You Can Paste Into Your SOP

| Step | Owner | Target | Evidence To Keep |

| Appointment recorded | Case lead | Day 0 | Appointing order PDF |

| Draft and review | Senior | Day 1 to Day 5 | Draft PDF, review notes |

| File to IRS | Case lead | Day 6 to Day 9 | Signed form, certified receipt |

| Receipt follow up | Admin | Day 20 to Day 30 | USPS delivery proof |

| Annual refresh if applicable | Case lead | Month 11 | New 56‑F packet |

| Termination filing | Case lead | Within 10 days of end | Termination order, filing proof |

Security, Recordkeeping, And Audit Readiness

Form 56‑F is small, but it carries authority. Treat it like any other control document.

- Store the packet in a controlled DMS folder with role‑based access.

- Use a standard file name pattern, for example FI‑EIN‑Form56F‑YYYYMMDD‑Initial or Termination.

- Keep a one‑page index at the front of the PDF that lists contents, dates, and the mailing tracking number.

- Maintain an activity log, who prepared, who reviewed, date mailed, and where mailed.

- If your institution uses an incident or issue tracker, create a 56‑F category so misdirected IRS mail can be tied back to filings quickly.

Where Accountably Fits, Only If You Need Hands‑On Help

If your in‑house team is underwater, you can outsource the busywork without losing control. On the Accountably side, we build disciplined, SOP‑driven delivery for CPA firms and financial institution teams. That can include preparing 56‑F packets from your templates, keeping the routing guide current, and maintaining the certified mail log, all inside your systems. We are not a resume shop, we are a structured delivery partner that works to your checklist and your deadlines, so you keep authority and visibility while moving faster.

Our goal is simple, give you capacity without chaos, so your staff spends time on tax positions and strategy, not chasing envelopes.

FAQs About IRS Form 56‑F

What is Form 56‑F used for, in plain terms?

It tells the IRS who has authority to act for a financial institution, for example an FDIC receiver. You file when the fiduciary begins, you file annually if you continue for refund purposes, and you file again when the role ends. This keeps IRS notices and refund matters pointed at the right party.

Is Form 56‑F the same as Form 56?

No. Form 56 covers general fiduciaries, like executors and trustees. Form 56‑F is narrow, it is for financial institutions with a federal agency acting as fiduciary, and it includes specific steps for refunds and consolidated groups.

Can I e‑file Form 56‑F?

No, mailing is required. Use certified mail, keep the tracking number, and save a clean PDF packet in your document system. If timing is sensitive, mail early in the 10‑day window and set a reminder to confirm delivery.

Where do I send it?

If you are filing for section 6402 refunds or section 6903 fiduciary notice, send it to the Service Center where the institution files its return. If you are filing under section 6036, send it to the Advisory Group Manager that covers the institution. Always confirm the current address before mailing.

What if the bank was in a consolidated group?

Follow the 56‑F instructions for consolidated return cases. You may need to copy the common parent and keep proof. Refund rights can be complex here, so document every step, who you notified, and why.

What happens if I file late?

Late filings cause misdirected mail and delays, and they can complicate refund claims. File as soon as you discover the gap, document why it was late, and tighten your SOPs so it does not happen again.

Tools, Templates, And A Clean Filing Kit

You can standardize 56‑F in a simple kit your team can grab during a busy week.

- Intake form, legal name, EIN, year end, appointment date, consolidated group status, contacts.

- Routing guide, which address for section 6402 and 6903 filings, which address for section 6036 filings, and a link to your internal address checker.

- Packet index template, lists each document, dates, and the certified mail tracking number.

- Filing memo, one page that states what was filed, when, why, and who signed.

- Annual tickler, a calendar reminder and a dashboard column in your case tracker.

Sample Packet Index You Can Copy

| Order | Document | File Name Example | Notes |

| 1 | Signed Form 56‑F | FI‑EIN‑Form56F‑20260315‑Signed.pdf | Original signature |

| 2 | Appointing order | FI‑EIN‑Order‑20260310.pdf | Certified copy if available |

| 3 | Insolvency or replacement order | FI‑EIN‑Order‑Insolvency‑20260310.pdf | If applicable |

| 4 | Consolidated parent notice | FI‑EIN‑ParentNotice‑20260315.pdf | If applicable |

| 5 | Certified mail receipt | FI‑EIN‑USPS‑9405‑XXXX.pdf | Add tracking number in file name |

Compliance Notes And YMYL Care

This topic affects taxes, refunds, and legal authority, so accuracy matters. Always verify the current Form 56‑F revision and where to file before you mail. If you face a complicated refund or consolidated group issue, talk with tax counsel or a consolidated return specialist. Nothing here is legal advice, it is practical guidance to help you run a clean process.

The safest habit is simple, verify the current form, confirm the filing address, mail within the 10‑day window, and keep proof.

Wrap Up And Next Steps

If you handle receiverships or advise on troubled bank situations, make Form 56‑F part of your standard open and close routines. File at appointment, refresh annually if needed, and terminate on exit. Keep a tight packet, and keep proof. This small form prevents big problems.

Simplify Delivery, Improve Margins, Stay in Control.

Offshore support that works exactly like your in-house team.

???? Let’s Talk