Scale Your CPA Firm Without Adding Headcount

Build your offshore team that works your way, trained, compliant, and white-labeled under your firm.

???? Book a Discovery CallTable of Contents

- Scale Your CPA Firm Without Adding Headcount

- Key Takeaways

- What Form 3468 Does, in Plain English

- Hundreds of Firms Have Already Used This Framework.

- What Changed Recently

- How This Post Is Structured

- The Parts of Form 3468, What Each One Covers

- Improve Margins Without Compromising Quality

- Part I, The Information You Must Get Right

- Who Files and How Pass‑Throughs Handle It

- Documentation That Protects the Credit

- Advanced Coal, Gasification, and Advanced Energy Projects

- Part III, Qualifying Advanced Energy Project Credit, Section 48C

- Records and Controls That Survive Review

- Rehabilitation Credit, Energy Credit, and the New Clean Electricity Credit

- Bonuses You Can Stack, With Care

- Reporting on Form 3800, Limits, Ordering, and Carryforwards

- Records and Workflow That Make Audits Boring

- FAQs

- Final Notes and a Simple CTA

- Simplify Delivery, Improve Margins, Stay in Control.

If you invest in qualifying property, Form 3468 is how you turn that investment into tax credit dollars, and Form 3800 is where those dollars are ultimately limited and applied.

Key Takeaways

- You use Form 3468 to compute investment credits across several areas, including the section 48 energy credit, the section 48E clean electricity investment credit for property placed in service after December 31, 2024, the section 48C advanced energy project credit, and the section 47 rehabilitation credit.

- Partnerships and S corporations compute credits at the entity level on Form 3468 and pass the details to owners, who then apply limits on Form 3800.

- Many energy projects follow a base 6 percent investment credit that increases to 30 percent if prevailing wage and apprenticeship requirements are satisfied or if an exception applies, with possible adders for domestic content and energy communities.

- Low‑income communities bonus credits can add 10 or 20 percentage points for qualifying small solar and wind facilities that receive an allocation.

- You aggregate credits on Form 3800, apply ordering and limitation rules, and carry unused general business credits back 1 year and forward 20 years.

What Form 3468 Does, in Plain English

Form 3468 converts qualifying capital spending into investment credits under the general business credit. Current instructions reflect Inflation Reduction Act changes and add the clean electricity investment credit under section 48E for property placed in service after 2024. If you are filing for a fiscal year that ends in 2025, section 48E may already appear on your form.

You complete Part I once for each facility or property, then complete the relevant part for the credit you are claiming. For many elections or transfers, you also need a pre‑filing registration number. Keep that number with your workpapers and return attachments.

When your entity is a partnership or S corporation, you still complete Form 3468 to compute credit amounts and provide line‑level information to owners. Owners then apply limits and ordering on Form 3800. This split between computation at the entity and limitation at the owner is where many review notes start, so align your K‑1 statements and activity tags early.

Hundreds of Firms Have Already Used This Framework.

Join the growing list of CPA and accounting firms using Accountably’s Offshore Playbook to scale faster.

???? Get Your FREE Playbook

???? Visit Jugal Thacker’s LinkedIn

Send him a connection request and message “Playbook” to get your copy.

What Changed Recently

- Part V adds the section 48E clean electricity investment credit, which covers qualified clean electricity facilities and qualified energy storage technology placed in service after 2024.

- Part VI, the section 48 energy credit, now explicitly lists technologies like energy storage technology, microgrid controllers, qualified biogas property, and more, along with the domestic content and energy community adders.

- The low‑income communities bonus program for small solar and wind facilities can add 10 or 20 percentage points if you receive an allocation and meet program timelines.

- Domestic content guidance now includes elective safe harbor tables that clarify component classifications and percentages you can rely on when certifying domestic content.

How This Post Is Structured

I will walk you through the parts of Form 3468 you are most likely to touch, what each section expects, and the documentation reviewers look for. I will also cover pass‑through reporting, Form 3800 limits, carryforwards, and practical checklists that cut rework. Where the rules changed for 2025 filings, I call that out so you can update your templates with confidence.

A Quick Word on Workflow

If your firm handles multiple energy projects, treat each facility as its own mini‑engagement. Name files consistently, store certifications and registration numbers in the same subfolder, and tie the asset record, placed‑in‑service date, and the Form 3468 part you used. That simple habit saves hours in review and protects the credit if you are audited.

We have seen firms cut review time by standardizing facility folders with five items, the registration letter, certifications, cost detail by component, placed‑in‑service proof, and a one‑page computation summary. That checklist keeps partners out of email hunts and in client strategy.

Light mention for fit, not a pitch, if you run lean during peak season, a structured offshore team can prepare those files inside your system and templates so your reviewers see a consistent package every time. That is the kind of delivery discipline Accountably builds for busy CPA firms. Use it only if it helps you hit deadlines without quality drift.

The Parts of Form 3468, What Each One Covers

Here is a simple map you can keep next to your workpapers. You always complete Part I once per facility or property, then add the relevant computation part.

Improve Margins Without Compromising Quality

Offshore staffing helps firms deliver more, scale faster, and stay compliant, without adding local headcount.

???? Book a Discovery Call| Part | What it covers | Typical users | Key paperwork |

| Part II, Section A | Qualifying Advanced Coal Project Credit, section 48A | Utilities, industrial projects | IRS or DOE‑related certifications, qualified investment basis detail |

| Part II, Section B | Qualifying Gasification Project Credit, section 48B | Industrial gasification projects | Certification letter, CO2 capture details if seeking 30 percent tier |

| Part III | Qualifying Advanced Energy Project Credit, section 48C | Manufacturers, recyclers, industrial decarbonization | Allocation letter, certification, placed‑in‑service notices |

| Part IV | Advanced Manufacturing Investment Credit, section 48D | CHIPS facilities | 48D specifics, elective pay where applicable |

| Part V | Clean Electricity Investment Credit, section 48E | Clean electricity facilities and energy storage after 2024 | Facility details, emissions or model info where required, registration number |

| Part VI | Energy Credit, section 48 | Solar, geothermal, fuel cells, storage, microgrid controllers, biogas, small wind, CHP | Domestic content and energy community statements if claimed |

| Part VII | Rehabilitation Credit, section 47 | Certified historic structures and qualified rehab expenditures | NPS approvals, QRE schedules, 5‑year ratable claim tracking |

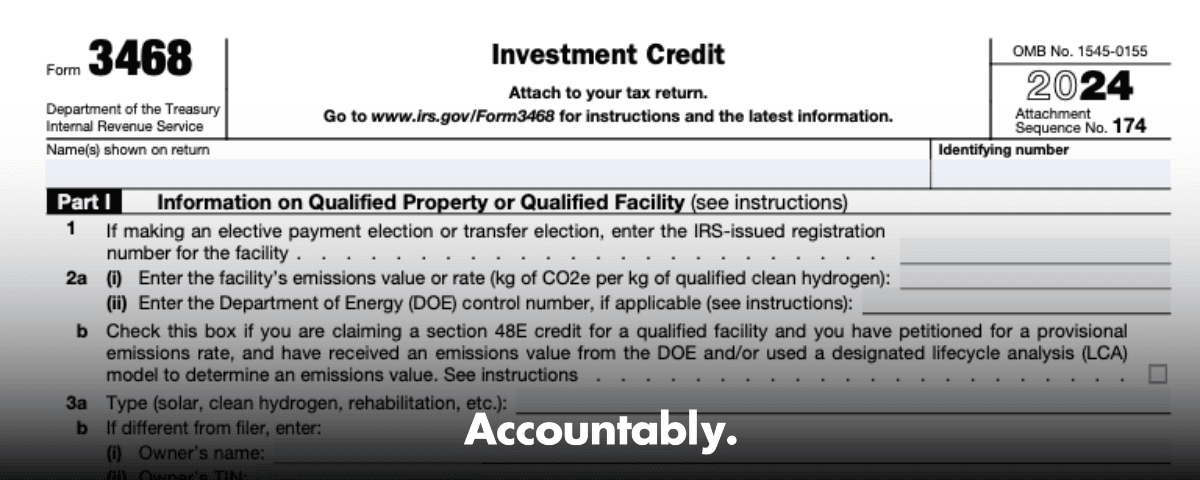

Part I, The Information You Must Get Right

Part I is where you identify the facility or property and enter the pre‑filing registration number if you intend to transfer a credit or make an elective payment election where allowed. Registration happens before you file, and it is required for transfers and certain elective payments. Save the registration acknowledgment with your form.

You will also indicate whether you are completing Part V or Part VI and whether prevailing wage and apprenticeship rules apply. If you are claiming domestic content or energy community adders, attach the required statements. Build templates for those statements so you do not reinvent them each time.

Pre‑Filing Registration, Transfers, and Elective Pay

- Pre‑file registration is required if you plan to transfer section 48, 48E, or 48C credits, or make elective payment elections where applicable. You receive a registration number that must appear on Form 3468 and Form 3800.

- Section 6418 transfers are available for sections 48, 48E, and 48C. Applicable entities may use section 6417 elective payment for certain credits, following the steps in the instructions.

Who Files and How Pass‑Throughs Handle It

C corporations claim credits directly against income tax. Partnerships and S corporations compute credits on Form 3468, then pass the data owners need on Schedules K and K‑1. The instructions list exactly which lines to complete so owners can compute their share, and they emphasize attaching a statement that provides facility‑level information. Owners then aggregate and limit credits on Form 3800.

Tax‑exempt or governmental applicable entities can treat certain investment credits as a payment of tax, which can generate refunds. When applicable, they file Form 3468, Form 3800, and their return, typically Form 990‑T, and must complete pre‑filing registration before making the election.

Documentation That Protects the Credit

Every number on Form 3468 should tie to a source document. For energy projects, keep invoices by component, interconnection costs, contractor certifications, and placed‑in‑service proof. For domestic content, attach the certification with the required details. For low‑income allocations, keep the control number and placed‑in‑service report. The instructions specify the statements that must be attached when claiming increased credit amounts.

A Reviewer’s Mini‑Checklist

- Registration number, facility name, and location match across Form 3468, Form 3800, and statements.

- Basis reconciles to the fixed asset subledger with in‑service dates.

- If you checked prevailing wage or apprenticeship boxes, attach the increased credit amount statement.

- If you claimed domestic content or energy community, attach the required certification statement and support.

Advanced Coal, Gasification, and Advanced Energy Projects

These parts are specialized, but when they apply, they are high‑value.

Part II, Advanced Coal Project Credit, Section 48A

The advanced coal project credit equals 20 percent, 15 percent, or 30 percent of qualified investment depending on project category under section 48A. Projects in the 30 percent tier generally include specified advanced coal‑based generation categories. These credits require certification and, for certain phases, CO2 separation and sequestration thresholds. Keep the certification letter and cost detail that proves qualified investment.

Part II, Qualifying Gasification Project Credit, Section 48B

The gasification credit is 20 percent of qualified investment, or 30 percent for allocated Phase II projects that capture and sequester at least 75 percent of total CO2 emissions. These credits also require certification and follow allocation rounds. Preserve the certification and engineering documentation with your return file.

Part III, Qualifying Advanced Energy Project Credit, Section 48C

Section 48C was refreshed and funded by the Inflation Reduction Act. It provides an investment credit for projects that re‑equip, expand, or establish facilities that manufacture or recycle clean energy components, reduce industrial emissions, or process critical materials. The base rate is 6 percent, which increases to 30 percent if prevailing wage and apprenticeship conditions are met. Credits are allocated through the IRS with DOE technical review. Do not place property in service before your allocation or you will be ineligible.

The 48C program includes strict timelines, commonly two years to meet certification and two more years to place in service. Track those dates on your close calendar and set reminder tasks so you do not miss a milestone.

Practical filing tips for Parts II and III

- Use a separate facility folder with the allocation or certification letter, capital detail schedules, and a placed‑in‑service memo.

- Tag each asset line with the statute section so it flows to the right part of Form 3468.

- For projects with CO2 capture thresholds, keep the test protocol and results with your cost file, not in a separate engineering drive.

Records and Controls That Survive Review

Whether your claim is under section 48A, 48B, or 48C, reviewers focus on three things, the certification, the basis, and the timing. Certification must match the project. Basis must be depreciable and integral to the project. Timing must align with allocation rules and placed‑in‑service dates. If your team keeps those three proof points in every facility folder, you will clear most review comments in a single pass.

Think in threes, certification, basis, timing. If any one is missing, the credit is at risk.

Light mention where it fits, if high‑volume prep stretches your staff, consider standardizing these facility folders. An offshore team that lives inside your workpapers can build and name them the same way every time so partners spend fewer hours in review and more time in advisory.

Rehabilitation Credit, Energy Credit, and the New Clean Electricity Credit

Part VII, Rehabilitation Credit, Section 47

For certified historic structures, the credit equals 20 percent of qualified rehabilitation expenditures, but you generally claim it ratably over five years for amounts paid or incurred after 2017. The old 10 percent pre‑1936 building credit no longer applies except under narrow transitional rules. Keep National Park Service certifications, your qualified rehabilitation expenditures schedule, and proof you met the substantial rehabilitation test.

Part VI, Energy Credit, Section 48

Part VI covers a broad set of energy properties, solar, geothermal, qualified fuel cells, small wind, combined heat and power, geothermal heat pumps, energy storage technology, qualified biogas property, microgrid controllers, and more. Section 48 works on a base and bonus model, 6 percent base that increases to 30 percent if you meet prevailing wage and apprenticeship requirements, or if an exception applies. Additional adders may apply for domestic content and energy communities. Track the statements you must attach when you claim increased credit amounts.

Part V, Clean Electricity Investment Credit, Section 48E

For property placed in service after December 31, 2024, section 48E becomes available for qualified clean electricity facilities and qualified energy storage technology. It follows similar base and bonus mechanics and introduces clean electricity definitions, including emissions concepts and designated lifecycle analysis models for certain technologies. If you are a fiscal‑year filer whose year ends in 2025, you may already see 48E on your form.

Bonuses You Can Stack, With Care

- Domestic content, if you meet the requirement, increases the applicable percentage by 10 percentage points if you meet prevailing wage and apprenticeship or another qualifying condition, otherwise by 2 points. New elective safe harbor tables help classify components and cost shares.

- Energy communities, you can increase the applicable percentage by 10 points when prevailing wage and apprenticeship apply, or by 2 points otherwise, for projects placed in service in an energy community.

- Low‑income communities bonus, for small solar and wind facilities with an IRS allocation, add 10 or 20 percentage points depending on category. Keep the control number and placed‑in‑service reporting.

A properly structured solar project can reach a total credit as high as 70 percent when base, domestic content, energy community, and low‑income bonuses apply, subject to program rules and allocations. Your documentation must support each adder and meet placement and certification timing.

Prevailing Wage and Apprenticeship, The Practical Bits

Prevailing wage and apprenticeship rules apply across several clean energy provisions. Use current wage determinations, maintain payroll records, and attach the increased credit amount statement when you check the box for increased rates.

Tip, keep a single PDF with wage determinations, contractor letters, and apprentice ratios for each facility. It travels with the asset file so review does not stall.

Example, Storage + Solar

- You place a 3 MW AC solar facility and a co‑located battery in service in 2025.

- You meet prevailing wage and apprenticeship, you qualify for the 30 percent base rate.

- If the site is in an energy community and you meet domestic content, you may add 10 points for each.

- If you also received a low‑income allocation because the project qualifies and is under 5 MW, you add 10 or 20 points. Document each element before you file.

Reporting on Form 3800, Limits, Ordering, and Carryforwards

After you compute credits on Form 3468, you aggregate them on Form 3800. The general business credit applies ordering rules and limits, including consideration of tentative minimum tax where relevant. Unused general business credits are carried back 1 year and forward 20 years, with special rules for certain credits. Apply carryforwards before current‑year credits, then apply any carryback. Keep a simple tracker so older amounts are used first.

Entity Coordination

If you are a partner or S corporation shareholder, your K‑1 statement should include the facility information your preparer used on Form 3468. You then report those amounts on your own Form 3800 and apply your personal limits and carryforwards. Aligning activity codes and facility names between the entity and owner returns removes a surprising amount of friction in review.

Records and Workflow That Make Audits Boring

- Facility folder, registration letter, certifications, allocation or control numbers, increased credit statements, domestic content statement if claimed, and placed‑in‑service proof.

- Basis support, invoices by component, contractor certifications, and interconnection costs with section 50 basis reduction applied where relevant.

- K‑1 statements that mirror Form 3468 line references for pass‑through owners.

Aim for two to four pages of computation and statements per facility, plus source documents. If your reviewer cannot find the registration number and the control number in 30 seconds, the package is not ready.

FAQs

What is Form 3468 used for, exactly?

It is the computation form for several investment credits, including sections 48, 48E, 48C, 48A, 48B, and 47. You attach it to your return, and you carry totals to Form 3800 where the general business credit limits apply.

How do section 48 and section 48E differ?

Section 48 applies to energy property like solar, geothermal, storage, microgrid controllers, and more. Section 48E is the clean electricity investment credit for qualified facilities and qualified energy storage technology placed in service after 2024. Both use base and bonus rates with potential adders.

Can I transfer these credits or use elective pay?

Yes. Eligible taxpayers may transfer section 48, 48E, and 48C credits under section 6418 after completing pre‑filing registration. Certain applicable entities can make elective payment elections under section 6417 for specified credits. Follow the sequencing in the instructions.

How is the rehabilitation credit claimed now?

For most projects, you claim 20 percent of qualified rehabilitation expenditures ratably over five years, and the pre‑1936 10 percent credit no longer applies except for narrow transitional cases. Track certifications and the substantial rehabilitation test.

What are the low‑income communities bonus credit rules in a sentence?

For small solar and wind facilities under 5 MW, an IRS allocation can add 10 or 20 percentage points if your facility meets one of four categories, low‑income community, Indian land, qualified low‑income residential building, or qualified low‑income economic benefit. Keep the control number and meet placed‑in‑service timelines.

How do carryforwards work if I cannot use the credit this year?

Unused general business credits generally carry back 1 year and forward 20 years. Form 3800 applies ordering rules, carryforwards first, then current‑year credits, then carrybacks. Maintain a schedule with origination year and expiration.

Final Notes and a Simple CTA

You already know the hard part is not finding opportunities, it is delivering them cleanly at scale. Build a repeatable facility folder, get pre‑filing registration done early when you plan to transfer or use elective pay, and keep your statements ready for domestic content, energy community, and increased credit amounts.

If you need structured help building those files inside your systems, Accountably integrates disciplined offshore teams who follow your templates, which keeps Form 3468 and Form 3800 packages consistent and your partners out of review loops. Use that only where it helps you protect quality, security, and turnaround.

Small disclaimer, this guide is general information, not tax advice. For specific credits, consult the current IRS instructions and a qualified tax professional.

Simplify Delivery, Improve Margins, Stay in Control.

Offshore support that works exactly like your in-house team.

???? Let’s Talk