Scale Your CPA Firm Without Adding Headcount

Build your offshore team that works your way, trained, compliant, and white-labeled under your firm.

???? Book a Discovery CallTable of Contents

- Scale Your CPA Firm Without Adding Headcount

- Key Takeaways

- What Form 8508 actually does

- Hundreds of Firms Have Already Used This Framework.

- When and where to send Form 8508

- Form 8508 vs. Form 8508‑I, and a note on IRIS

- Improve Margins Without Compromising Quality

- Step‑by‑step completion guide

- Step‑by‑step completion guide, continued

- When to file, where to send, and how the IRS evaluates it

- What forms are covered, exactly

- Special cases worth calling out

- Real‑world examples

- Common mistakes that slow or sink a waiver

- Where to get and send the form

- A simple checklist you can print

- Quick templates you can adapt

- FAQs

- Field‑tested tips from our year‑end desk

- If capacity is your roadblock, not the rules

- Final word and next steps

- Simplify Delivery, Improve Margins, Stay in Control.

The fix was Form 8508, the IRS waiver from mandatory e‑filing, filed on time and with the right boxes checked. If you are in the same spot, this guide walks you through what to do, when to do it, and how to avoid costly rework.

If you must e‑file but can’t, Form 8508 is your path to a one‑year waiver for specific information returns under your TIN, provided you submit it on time and follow the rules.

Key Takeaways

- Form 8508 is the IRS waiver request from mandatory e‑filing for specific information returns under a single TIN for one tax year. It covers W‑2 series, 1042‑S, 1097‑BTC, 1098 and 1099 series, 3921/3922, 5498 series, 8027, and ACA Forms 1094‑C/1095‑B/1095‑C.

- File it early. The IRS encourages filing at least 45 days before the return due date and begins processing on January 1 of the calendar year the returns are due. Fax is preferred, or mail to the Kearneysville, WV address.

- The 10‑return rule is aggregated across many information returns, so nine 1099s plus a few W‑2s can push you into e‑file territory. Penalties for failing to e‑file without a waiver can reach up to $340 per return.

- If a waiver for original returns is approved, corrections of the same type are covered. If you e‑file originals but want to paper file only corrections, you must request a corrections‑only waiver.

- Reasons that can support a waiver include undue financial hardship, first year of business, federally declared disaster, serious illness, religious beliefs, rural filers without internet, and limited digital literacy, among others recognized in IRS internal guidance.

What Form 8508 actually does

Form 8508 lets you ask the IRS for a one‑year waiver from electronic filing for specified information returns tied to the TIN on the form. One request can cover multiple return types, but it applies only to the forms you check in Block 5 for that TIN and that tax year. The IRS treats the mandate broadly. If you file 10 or more information returns in a calendar year, counted in the aggregate across common types, you generally must e‑file unless you have an approved waiver.

Which forms are covered? The list includes the W‑2 series, the full 1099 and 1098 families, 1042‑S, 3921/3922, 5498 series, 1097‑BTC, 8027, plus ACA Forms 1094‑C/1095‑B/1095‑C. The waiver lasts one year and is TIN‑specific. If the IRS grants any of these waivers, it automatically applies to Forms 8300 for that calendar year, though you cannot request a waiver solely for Forms 8300.

Hundreds of Firms Have Already Used This Framework.

Join the growing list of CPA and accounting firms using Accountably’s Offshore Playbook to scale faster.

???? Get Your FREE Playbook

???? Visit Jugal Thacker’s LinkedIn

Send him a connection request and message “Playbook” to get your copy.

Practical example: Your firm plans to e‑file 1095‑C but has a short‑term systems issue with 1099‑NEC and W‑2G. You can request a waiver that lists 1099‑NEC and W‑2G counts in Block 5. The approval, if granted, covers only those types for that TIN in the current year.

When and where to send Form 8508

Timing is everything. The IRS encourages you to submit at least 45 days before your returns are due. For January 31 due dates, that means aiming by mid‑December. The IRS does not process waiver requests before January 1 of the year the returns are due, so plan accordingly and keep proof of submission.

How to submit

- Fax, preferred by the IRS, to 877‑477‑0572 in the U.S., or 304‑579‑4105 internationally.

- Or mail to: Internal Revenue Service, Attn: Extension of Time Coordinator, 240 Murall Drive, Mail Stop 4360, Kearneysville, WV 25430. Submit by one method only, and keep your confirmation.

Penalty reminder: If you were required to e‑file and did not, and you lack an approved waiver, the IRS may assess up to $340 per return. Pair your process with a calendar reminder so your request lands on time.

Form 8508 vs. Form 8508‑I, and a note on IRIS

- Use Form 8508 for the information returns listed above, including ACA Forms 1094‑C/1095‑B/1095‑C.

- Use Form 8508‑I only to request a waiver for Form 8966 (FATCA Report).

If you file via the IRS Information Returns Intake System, IRIS, the paper form still governs the waiver request. The current form instructions note that for a corrections‑only waiver, IRIS filers should leave the corrections box blank on the paper form. This nuance matters when your originals are e‑filed in IRIS but you want permission to paper‑file corrections.

Improve Margins Without Compromising Quality

Offshore staffing helps firms deliver more, scale faster, and stay compliant, without adding local headcount.

???? Book a Discovery CallStep‑by‑step completion guide

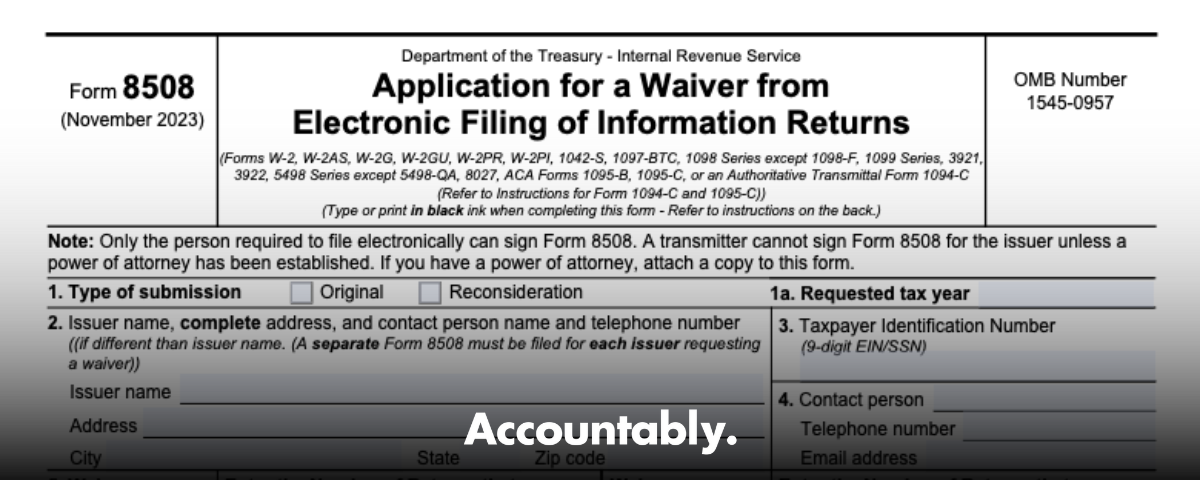

Block 1, submission type

Pick Original for your first waiver request for the current tax year. Choose Reconsideration only if the IRS denied or has not decided your earlier request and you are sending new documentation, still within the same tax year window. File at least 45 days before the due date.

Blocks 2–4, issuer and contact

Enter the legal name, full mailing address, and the correct TIN for the filer, plus a reachable contact with phone and email. The waiver is per TIN, so verify the number carefully.

| Field | What to get right |

| Issuer name and address | Match legal records, include ZIP+4 when available |

| TIN | Nine digits that match IRS records |

| Contact | Direct phone and monitored email |

Keep paragraphs short in your justification later and make sure an authorized person signs.

Block 5, the forms and the counts

Check each return type you want covered and enter two numbers for each, this year’s expected paper filings and next year’s expected paper filings. The IRS uses these counts to scope your waiver. Missing a form here means it is not covered later.

Step‑by‑step completion guide, continued

Block 5, the forms and the counts

Check every return type you want covered, then add two numbers for each, how many you expect to file on paper this year and how many next year. The IRS scopes your waiver to the exact items you mark in Block 5, so if it is not checked, it is not covered. One Form 8508 can include several return types for the same TIN.

Practical tip: build your list from last year’s activity plus current year changes, for example, new contractors that add 1099‑NEC, a new entity that adds W‑2 or 1095‑C, or a stock plan event that triggers 3921 and 3922. If you are unsure about volumes, enter a reasonable estimate. The IRS expects approximations, not exact counts.

Block 6, corrections‑only

Mark “Yes” only if you want a waiver that applies to corrected returns when your original returns will be e‑filed. If you request and receive a waiver for original returns, corrections of that same type are already covered. IRIS filers should leave Block 6 blank on the paper form, this note appears right on the form.

Request a corrections‑only waiver when you e‑file originals but need permission to file only your corrections on paper. Originals that are waived automatically cover corrections for that type.

Block 7, first‑time request

If this is your first‑ever waiver request for any of the forms you checked in Block 5, select “Yes” and skip to the signature line. The IRS states that your first request will be automatically granted for the current year. If you have requested a waiver in the past, select “No” and include your justification.

Block 8, justification and cost estimates

Only complete Block 8 when your request is based on undue financial hardship. You must attach two current cost estimates from third parties, for example software, programming, or service bureau fees to produce an e‑file. Estimates from prior years are not accepted. Other acceptable reasons do not require the cost estimates, for example disaster impact, serious illness, first year of business, or a foreign filer unable to obtain software.

Model language for your attachment

- We are requesting a waiver due to undue financial hardship. Enclosed are two current cost estimates for software and third‑party preparation needed to comply with the e‑file requirement. These costs exceed our costs to produce paper filings for the current year.

- Our business experienced a declared disaster that disrupted records and systems needed to e‑file. We can file correct paper returns by the deadline.

- This is our first year of operations. Our systems and staffing are not yet prepared to e‑file, and we will comply via paper filing this year.

Block 9, signature

The taxpayer, or a person authorized to sign legally binding documents for the taxpayer, must sign. A transmitter cannot sign unless there is a valid power of attorney attached.

When to file, where to send, and how the IRS evaluates it

- File at least 45 days before the due date of the information returns you want covered. Requests are processed beginning January 1 of the calendar year the returns are due.

- Fax, preferred by the IRS, to 877‑477‑0572 in the U.S., or 304‑579‑4105 internationally. Or mail to: Internal Revenue Service, Attn: Extension of Time Coordinator, 240 Murall Drive, Mail Stop 4360, Kearneysville, WV 25430. Send by one method only. Keep your confirmation.

- The waiver applies to the current year and to the specific forms you checked for the TIN on the request. If you need a waiver next year, reapply.

Penalty note: if you are required to e‑file, you fail to do so, and you do not have an approved waiver, the IRS may assess a penalty. In 2025 instructions for information returns, the maximum standard penalty tier reaches $340 per return for filings very late or never filed, and penalties for failure to e‑file apply only to the count above the 10‑return threshold. Amounts are indexed and can change, so check the current general instructions.

A simple date planner for January deadlines

| Scenario | Return due | Waiver timing target | Latest practical send date |

| W‑2, 1099‑NEC due Jan 31 | Jan 31, 2026 | Mid‑December 2025 | Early January 2026, noting IRS begins processing Jan 1 |

| 1095‑C due Feb/March, electronic | Spring 2026 | At least 45 days prior | Mid‑January 2026 |

Always keep proof of fax or certified mail. If you cut it close, include a brief cover page with your contact info so TSO can reach you quickly.

What forms are covered, exactly

Form 8508 covers the W‑2 family, 1042‑S, 1097‑BTC, 1098 series except 1098‑F, 1099 series except 1099‑QA, 3921, 3922, 5498 series except 5498‑QA, 8027, and ACA Forms 1095‑B, 1095‑C, plus the authoritative 1094‑C transmittal. The approval is TIN‑specific and current‑year only. Use Form 8508‑I only for Form 8966, FATCA.

Special cases worth calling out

Religious‑belief exemption

If using the required technology conflicts with your religious beliefs, you are exempt from e‑filing. You do not have to file a waiver, although you may file Form 8508 with a statement so the IRS records the exemption. Keep documentation in your files in case of a penalty notice.

Corrections and IRIS

The e‑file mandate does not apply separately to originals and corrections. If your originals must be e‑filed, then corrections must be e‑filed too unless a corrections‑only waiver is approved. IRIS filers leave Block 6 blank on the form.

Real‑world examples

- Systems outage, January 20. Your payroll team can print W‑2s, but your SSA e‑file uploader will not be restored in time. You file Form 8508 by fax with a short note and, if needed, two cost estimates from vendors to produce an electronic file this season. You receive the approval letter and mail W‑2s.

- First year of operations. Your company opened in August. You check Yes in Block 7, skip Block 8, sign, and fax the request. The first‑time request is automatically granted for the current year.

- Corrections‑only. You e‑filed 1095‑C originals, then discovered TIN errors on a small subset. You want to send paper corrections. You request a corrections‑only waiver in Block 6.

Common mistakes that slow or sink a waiver

- Missing signature or missing cost estimates for a hardship‑based request. The IRS will deny it.

- Checking the wrong forms in Block 5, then asking to paper file a form that was not checked. Only marked forms are covered.

- Filing too late. Aim for at least 45 days before your due date. The IRS begins processing on January 1 of the filing year.

- Mixing submission methods. Use fax or mail, not both. Keep your submission receipt.

Where to get and send the form

Download the current fillable PDF of Form 8508 and follow the two‑page instructions on the back. Submit by fax or mail only, and keep your proof of submission and approval letter with your year‑end binder. If you are filing Form 8027 on paper under an approved waiver, include a copy of the waiver with those paper Forms 8027.

A quick word on support If your firm’s roadblock is not knowledge but capacity, structure, or review time, you are not alone. We have seen firms stall because delivery becomes the ceiling. Accountably operates as a U.S.‑led offshore partner that builds disciplined delivery with SOPs, structured workpapers, and multi‑layer review. If you need help with standardized workpapers, clean review notes, or meeting hard year‑end deadlines without burning out your team, talk with us about a controlled delivery model, not resume farming. Keep client trust high and your advisory time protected. (We mention this only where useful, since this guide is primarily educational.)

A simple checklist you can print

Use this to keep your request clean, complete, and on time.

- Confirm you actually need a waiver. Total your information returns across types to see if you hit the e‑file threshold.

- Pick your return types. List every form family you want covered in Block 5.

- Choose your submission type in Block 1. Original for a first request this year. Reconsideration only if you are adding new support after a denial.

- Complete issuer details in Blocks 2–4. Match legal name, address, and TIN, and add a reachable contact.

- Decide on corrections. If you will e‑file originals but want paper for corrections, mark Block 6.

- First‑time filer. If this is your first waiver for the forms you checked, set Block 7 to Yes.

- Hardship request. If Block 7 is No and you claim undue financial hardship, add two current cost estimates and a short explanation in Block 8.

- Signature. Have an authorized person sign and date in Block 9.

- Submit once by fax or mail. Keep your confirmation and a copy of the packet.

- Track the response. File the approval letter with your year‑end binder and share it with payroll or AP.

Timeline at a glance

| Task | Target date | Tip |

| Estimate counts and forms | Early December | Pull last year’s register plus current year changes |

| Prepare justification and quotes, if needed | Mid December | Get two current quotes if claiming hardship |

| Send Form 8508 packet | At least 45 days before due date | Fax once, save confirmation |

| Monitor mailbox and email | Ongoing | Watch for IRS reply and note any clarifications |

| File returns on paper if approved | By the original due date | Include a copy of the waiver with any 8027s you mail |

Quick templates you can adapt

Cover sheet

Subject, Form 8508, Waiver Request for [TIN], [Tax Year] We request a waiver from electronic filing for the checked information returns in Block 5 for [Tax Year]. Contact [Name, Title], [Phone], [Email] with any questions. We are submitting this request at least 45 days before the due date.

Hardship note

We request a waiver due to undue financial hardship. Enclosed are two current cost estimates for software and service bureau fees needed to produce valid electronic files. These costs exceed our ability to implement in time for this filing season. We will file correct paper returns by the deadline.

FAQs

What is Form 8508?

Form 8508 is the IRS request for a one‑year waiver from mandatory e‑filing of certain information returns under a single TIN. You list the return types you want covered, sign, and submit by fax or mail at least 45 days before the due date. If approved, you can paper file those returns for that year. Always check the current IRS instructions for any changes.

Is a first‑time request really simpler?

Yes. If this is your first waiver for the forms you checked, you mark first‑time in Block 7, skip hardship cost estimates, sign, and send. Still file early and keep proof, because the approval applies only to that tax year and TIN.

What if my originals are e‑filed but only corrections need paper?

Ask for a corrections‑only waiver in Block 6. If your waiver covers originals, corrections are automatically covered for that type. If originals are e‑filed, you need permission to mail corrections.

Who must file Form 8948?

Paid preparers file Form 8948 when they are required to e‑file an individual income tax return but cannot, usually because the taxpayer opts out or a valid exception applies. It documents why a paper submission is allowed. Review the current Form 8948 instructions for the specific criteria.

What is IRS Form 8832 used for?

Form 8832 lets eligible entities choose or change their federal tax classification, for example partnership to corporation. If you want S corporation status, use Form 2553 instead. Confirm effective dates and late election relief in the current instructions.

Who needs to file Form 8858?

U.S. persons that directly, indirectly, or constructively own certain interests in foreign disregarded entities or foreign branches file Form 8858. It reports the entity’s activities and the U.S. owner’s information. Because this is a complex international filing, check thresholds and definitions with current guidance.

What happens if my waiver is denied?

You must e‑file the covered returns by their due date or extended due date. If you believe the denial missed a fact, you can submit a reconsideration with additional documentation within the same tax year window. Keep your timeline tight, and consider alternate e‑file paths if the deadline is close.

Do states honor an IRS waiver?

An IRS waiver covers only federal filings. Some states have their own e‑file mandates and waiver processes. Check each state’s rules, especially for W‑2 and 1099 reporting.

Field‑tested tips from our year‑end desk

- Build a single counts sheet. Tally W‑2, 1099 families, 1042‑S, 1095‑B/C, and anything unusual like 3921 or 3922. This prevents gaps in Block 5.

- Lock your signer early. Calendar a 20‑minute slot so the signature and send do not slip.

- Keep a copy with your binder. If a notice arrives in summer, you can respond fast with proof.

- Pair the waiver with clean workpapers. Reviewers move quicker when schedules, naming, and versioning are consistent.

If capacity is your roadblock, not the rules

If the form itself is clear but your team is underwater, you may need structure, not more hours. At Accountably, we integrate trained offshore teams into your systems with SOP‑driven execution, standardized workpapers, and multi‑layer review so partners are not trapped in review loops. If you want production stability for busy season while protecting quality and security, we can help design a delivery model that holds up at scale. Brief chat, clear scope, documented workflow, and steady turnaround.

Final word and next steps

You now have the playbook. Confirm that you need a waiver, choose the forms, fill the boxes, include any required support, and send it at least 45 days before your due date. Save your proof, track the response, and file on time. If this is your first year, use the first‑time path. If only corrections need relief, request that specifically. Do the simple things right and you will reduce risk, keep clients informed, and move through year‑end with fewer surprises.

Simplify Delivery, Improve Margins, Stay in Control.

Offshore support that works exactly like your in-house team.

???? Let’s Talk