Scale Your CPA Firm Without Adding Headcount

Build your offshore team that works your way, trained, compliant, and white-labeled under your firm.

???? Book a Discovery CallTable of Contents

- Scale Your CPA Firm Without Adding Headcount

- Key Takeaways

- Who This Is For, And How To Use It

- Hundreds of Firms Have Already Used This Framework.

- What Form 8864 Covers

- Timing, The Sale‑Or‑Use Year Controls

- Improve Margins Without Compromising Quality

- Credit Components Under Section 40A

- Section 40B, Sustainable Aviation Fuel Credit, What To Prove

- Who Must File Form 8864

- When To Claim The Credit

- Software Workflows, ProConnect Tax

- Software Workflows, TaxSlayer Pro

- Attachment Requirements And Diagnostic Ref. #10568

- Reporting Credits On Form 3800 When You Do Not File 8864

- Year‑Specific Context For 2025 Planning

- Accuracy Checks And Saving Your Return

- Practical Examples, Micro Scenarios You Can Paste Into SOPs

- Review Protection And Delivery Discipline

- Additional Resources And Related Articles

- FAQs

- Conclusion

- Simplify Delivery, Improve Margins, Stay in Control.

Quick empathy check Most firms do not struggle because of a lack of clients, they struggle because delivery gets messy. Review loops, missing attachments, and unclear ownership turn simple credits into bottlenecks. The fix is structure, not heroics.

Key Takeaways

- Form 8864 is used to claim section 40A biodiesel and renewable diesel credits and the section 40B sustainable aviation fuel, SAF, credit, based on the year the fuel is sold or used.

- Partnerships, S corporations, cooperatives, estates, and trusts file Form 8864 when they generate the credit. If you only receive a passthrough share, you generally report on Form 3800.

- Compute each section 40A component separately, biodiesel, renewable diesel, biodiesel mixture, renewable diesel mixture, and small agri‑biodiesel producer, then total them.

- Attach required certificates or statements. If your e‑file system cannot include PDFs, generate Form 8453 and mail the support promptly.

- Missing certificates often trigger software diagnostics such as ref. #10568. Clear it by attaching the biodiesel certificate and, if applicable, the reseller statement.

- For 2025 activity, confirm whether the 40A and 40B windows apply to your facts or whether the transaction belongs under the newer clean fuel production framework. Always check the return year first.

Who This Is For, And How To Use It

This guide is for managing partners, ops leads, senior tax managers, and software admins who want a calm, accurate 8864 workflow that holds up under review. You will get, in plain language, the timing rules, component breakdowns, documentation checklists, and step‑by‑step entries in ProConnect Tax and TaxSlayer Pro. I will also show you simple ways to avoid common rework, for example mismatched gallons and missing attachments that force last‑minute scrambles.

Why Delivery Breaks On 8864, And How To Avoid It

If your team is buried in compliance, it is easy for workpapers to get rushed and naming to drift. That leads to longer reviews and missed deadlines. Here is the simple fix.

- Define who requests certificates, who ties out gallons, who attaches PDFs or triggers 8453, and who runs final diagnostics.

- Standardize file names and version control for every certificate and reseller statement.

- Use a short, repeatable checklist per return so reviewers do not hunt for the same items twice.

A quick note, some firms add structured offshore capacity for seasonal spikes. When done with SOPs, layered review, and strict security, it removes chaos instead of adding it. On Accountably.com, we only bring this up where it truly helps, a disciplined offshore delivery layer can keep 8864 attachments, naming, and SLAs tight inside your own systems so partners spend time on strategy, not file wrangling.

Hundreds of Firms Have Already Used This Framework.

Join the growing list of CPA and accounting firms using Accountably’s Offshore Playbook to scale faster.

???? Get Your FREE Playbook

???? Visit Jugal Thacker’s LinkedIn

Send him a connection request and message “Playbook” to get your copy.

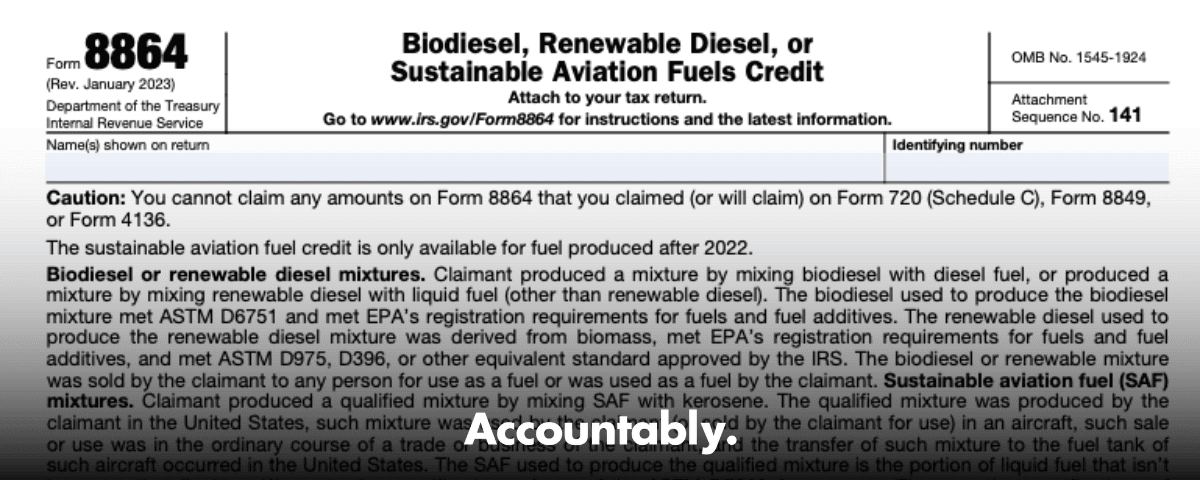

What Form 8864 Covers

Although there is just one form, it carries two regimes.

- Section 40A, biodiesel and renewable diesel credits, reported by component, biodiesel, renewable diesel, biodiesel mixtures, renewable diesel mixtures, and the small agri‑biodiesel producer credit.

- Section 40B, the sustainable aviation fuel credit, SAF, which is based on lifecycle greenhouse gas reduction in a qualified mixture for the eligible window.

You file Form 8864 to show eligibility, quantify gallons, compute each component correctly, and carry the credit to your return. If your only source is a passthrough K‑1, you generally skip 8864 and use Form 3800.

One‑Credit Rule

You cannot claim two different credits on the same gallons. Coordinate 8864 with Forms 720, 8849, and 4136 so you do not double claim. Make that reconciliation part of your review checklist.

Timing, The Sale‑Or‑Use Year Controls

Claim section 40A and 40B credits in the tax year the fuel is sold or used. Production dates, payment dates, and inventory movements do not control the 8864 claim. For mixtures, claim only the qualifying biodiesel or renewable diesel gallons you blended and then sold or used in that same tax year. Passthrough owners align to the passthrough’s sale‑or‑use year shown on the K‑1.

Pro tip Put the sale or use date in your certificate tie‑out worksheet. When deadlines hit, that single column saves you from second‑guessing the year.

Improve Margins Without Compromising Quality

Offshore staffing helps firms deliver more, scale faster, and stay compliant, without adding local headcount.

???? Book a Discovery CallCredit Components Under Section 40A

You must compute and report each 40A component separately before totaling them. That detail protects eligibility, accuracy, and downstream carryovers.

Biodiesel Credit

- Qualifying fuel, monoalkyl esters meeting EPA registration and ASTM standards.

- Documentation, Certificate for Biodiesel from the producer or importer, matched to your gallons, supplier name, and EIN.

- Common snag, entries rounded in software, gallons unrounded on the certificate. Tie out to at least two decimals and note your rounding rule in workpapers.

Renewable Diesel Credit

- Qualifying fuel, liquid fuel from biomass that meets applicable diesel specifications.

- Documentation, keep certificates and any statements that show the fuel meets registration and standard requirements.

- Common snag, crew assumes all renewable fuel is “renewable diesel.” Confirm the spec and the certificate language before you code it.

Mixture Credits, Biodiesel And Renewable Diesel

- Requirement, you must produce a qualified mixture and then sell or use it as fuel in a trade or business during the tax year.

- Claim only the biodiesel or renewable diesel gallons in the mixture.

- Watchlist, aviation blends have their own specifications, so read your supplier docs carefully.

Small Agri‑Biodiesel Producer Credit

- Confirm the producer meets the IRS size definition and observe the per‑gallon cap.

- Keep proof of capacity, ownership structure, and facility details with the file. Reviewers will ask.

Section 40B, Sustainable Aviation Fuel Credit, What To Prove

The SAF credit rests on lifecycle greenhouse gas reduction, GHG, for SAF in a qualified mixture over the eligible window. The base amount applies at a minimum threshold, and a supplemental amount increases the credit per percentage point above that threshold up to a cap. Your file needs three things, lifecycle support, SAF certifications that tie to the mixture, and the right producer, blender, or reseller statements.

SAF Documentation Pack

- Lifecycle analysis support, tied to the batch or certificate.

- Certificate for SAF synthetic blending component where applicable, and any required declarations.

- Reseller statements, if the chain requires them.

- A one‑page summary in your workpapers that reconciles gallons, lifecycle reduction, and the claimed per‑gallon amount.

Blockquote Keep the first certificate and declaration you rely on, then reference it cleanly in later claims. Reviewers hate hunting through last year’s archive. Future you will thank present you.

Who Must File Form 8864

File Form 8864 if you are a partnership, S corporation, cooperative, estate, or trust that directly generates section 40A or 40B credits in the sale‑or‑use year. If your only source is a passthrough, report on Form 3800 and keep the K‑1 statements with your records.

Passthrough‑Only Reporting, The No‑Duplication Rule

- Do not file your own 8864 if the credit comes only from a passthrough.

- Enter each component separately on Form 3800 so ordering and carryforward limits apply correctly.

- If you directly generate any portion of the credit, you must file Form 8864 for that portion.

When To Claim The Credit

The controlling rule, you claim 40A and 40B credits in the tax year the fuel is sold or used. This applies to each component, biodiesel, renewable diesel, biodiesel mixture, renewable diesel mixture, and small agri‑biodiesel producer. Align your claim to the sale or use date even if production or blending happened earlier.

Credit Timing Rules, A Simple Checklist

- Identify the sale or use date, then tag it to the tax year.

- File Form 8864 for that year if you are the entity that generated the credit.

- If e‑file will not carry PDFs, check the e‑file box to generate Form 8453 and mail the attachments.

- Retain all certificates and statements used to compute the claim.

Sale Or Use Year Examples

- You blended a biodiesel mixture on December 20 and sold it on January 3. The claim belongs in the year that includes January 3.

- You purchased renewable diesel in March and used it in production in April. Claim in the year that includes April’s use.

Passthrough Timing

Passthrough entities file Form 8864 for the year of sale or use and issue owner allocations on Schedule K‑1 for that same year. Owners report those amounts on their own Form 3800 for the same year. Do not duplicate the claim by also filing 8864.

Software Workflows, ProConnect Tax

You can generate and complete Form 8864 directly in ProConnect.

Where To Enter

- Open Input Return, then Credits, General Business and Vehicle Cr.

- Select the Energy or Fuel Production tab.

- Scroll to the Biodiesel and Renewable Diesel Fuels Credit, 8864, section.

- Enter the exact amounts for “Biodiesel, other than agri‑biodiesel,” and complete all other applicable fields, including mixtures and SAF if present.

Clearing Diagnostic Ref. #10568

If Diagnostic ref. #10568 appears, the software is telling you a required biodiesel certificate or reseller statement is missing. Clear it by attaching the PDF in the File Return tab, or check the e‑file option to generate Form 8453 and mail the support. Re‑run diagnostics to confirm it is cleared before you transmit.

Save, Re‑Open, Confirm

After populating the 8864 section, save the return, close the screen, and re‑open to confirm entries persisted and totals flow to the form. This tiny habit prevents the most common review surprise, empty fields after a refresh.

Blockquote Most rework on 8864 is not math, it is attachments. Match the certificate to the gallons, then attach, then save. In that order.

Software Workflows, TaxSlayer Pro

If your credits come directly from your activity, you will enter Form 8864 in TaxSlayer Pro rather than relying solely on Form 3800.

Where To Enter

- From the 1040 Main Menu, select Credits.

- Choose General Business Credits, then Current Year General Business Credits.

- In the Energy or Fuel Production area, select Form 8864.

- Enter each component, biodiesel, renewable diesel, mixtures, and small agri‑biodiesel producer.

Attachment Prompts And 8453

TaxSlayer Pro will prompt you to attach the Certificate for Biodiesel and, if applicable, the Statement of Biodiesel Reseller. If you cannot attach a PDF in the e‑file, generate Form 8453 and mail the documents. Keep a copy and proof of mailing in the file.

Accuracy Checks Before You File

- Run the accuracy check or diagnostics to confirm every required 8864 field is complete.

- Tie the Biodiesel, other than agri‑biodiesel, line to the certificate’s gallons and supplier info.

- Confirm you chose one submission method, either attach PDFs or use 8453, and apply it consistently.

Attachment Requirements And Diagnostic Ref. #10568

Diagnostic ref. #10568 usually flags that the biodiesel certificate or reseller statement is missing for a claim you entered. Treat it as a hard stop, not a suggestion.

Required Supporting Documents

- Certificate for Biodiesel that matches supplier name, EIN, gallons, and fuel type on your return.

- Statement of Biodiesel Reseller, if the supply chain requires it for your claim.

- For SAF, retain lifecycle support, SAF certifications, and any required declarations.

PDF Attachment Process

- Complete the 8864 inputs first.

- Save the return, then attach a legible PDF labeled to match the taxpayer and tax year.

- Confirm the attachment appears in the electronic return package.

- Re‑run diagnostics to clear ref. #10568.

Form 8453 Alternative

When you cannot include PDFs in the e‑file, select the option to generate Form 8453, print it, and mail the certificate or statement. Track the date mailed in your workpapers and keep proof of mailing.

Blockquote Pick one path, PDF in the e‑file or Form 8453 with mailed support. Mixing methods across engagements creates avoidable follow‑up and review confusion.

Reporting Credits On Form 3800 When You Do Not File 8864

If your only biodiesel, renewable diesel, or SAF credits come from passthroughs, go straight to Form 3800. You do not file Form 8864 yourself.

How To Report

- Use the passthrough’s K‑1 and attached statements to capture each component, biodiesel, renewable diesel, mixtures, small agri‑biodiesel producer, and SAF.

- Enter them on the appropriate Form 3800 lines so general business credit ordering and carryforward rules apply correctly across all credits.

- Keep the K‑1 and allocation statements with your workpapers. The IRS can ask for them even when you do not file 8864.

Preventing Duplicates

Confirm whether the passthrough already filed Form 8864 and attached certificates. You should never duplicate the claim by filing 8864 yourself for the same gallons. Trace the amounts to your Form 3800 and document the year alignment in your binder.

Year‑Specific Context For 2025 Planning

You will see questions this season about what changed. Here is a simple way to frame it for clients and your team.

- 8864 remains the path for 40A biodiesel and renewable diesel and 40B SAF claims that fall within their eligible windows based on the year of sale or use.

- For 2025 and later, many fuel incentives move into a production‑based regime with different forms, claimants, and documentation. When preparing 2025 returns, confirm which rules apply to your client’s fact pattern before you start data entry.

- Train your reviewers to ask one question up front, is this a 2024 sale or use, or a 2025 production claim. That single question prevents hours of rework.

8864 vs. Producer‑Based Credits, At A Glance

| Item | 8864, Section 40A/40B | Producer‑Based Regime, High Level |

| Core measure | Gallons sold or used in the tax year | Production at a qualified facility |

| Typical claimant | Blenders, sellers, or users under 40A, qualified SAF claimants under 40B | Domestic producers at registered facilities |

| Documentation | Biodiesel certificate, reseller statement, SAF lifecycle and certifications | Facility registration, emissions factors, production records |

| Filing artifact | Form 8864 with attachments or Form 8453 mailing | Separate form package per facility and year |

Note, laws can change. Always check current IRS instructions for the exact return year you are filing and adjust your workflow accordingly.

Accuracy Checks And Saving Your Return

Accuracy is built on habits, not heroics. Use this quick loop before you move on.

- Verify support

- Attach the certificate or reseller statement as a PDF in your e‑file package, or select the option to generate Form 8453 for mailing.

- Confirm method

- Choose PDF attachment or Form 8453 and apply it consistently across the return. Do not mix paths accidentally.

- Retain records

- Keep copies of every certificate, statement, and lifecycle analysis in a clean folder with year and taxpayer labels.

Practical Examples, Micro Scenarios You Can Paste Into SOPs

Example 1, Biodiesel Mixture Sold In January

- Facts, you blended a biodiesel mixture on December 20, 2024 and sold it January 5, 2025.

- Result, the claim aligns to the 2025 tax year only if the law allows credit for that year. If the window ended in 2024, you do not claim under 8864 for the January sale. Document the sale date, then confirm eligible regime before entering data.

- Documentation, attach the biodiesel certificate and reseller statement as needed.

Example 2, Renewable Diesel Used In A Trade Or Business

- Facts, renewable diesel was purchased in May and used in company trucks in June.

- Result, claim in the tax year that includes the June use.

- Documentation, certificate shows gallons and supplier EIN. Tie out to your usage records or purchase documents.

Example 3, Passthrough Owner

- Facts, you receive a K‑1 from a cooperative with allocations for biodiesel, renewable diesel mixture, and SAF.

- Result, you do not file 8864. Report each component on Form 3800 for the same tax year shown on the K‑1.

- Documentation, retain the K‑1, allocation statement, and a copy of the cooperative’s 8864 summary if provided.

Review Protection And Delivery Discipline

If your firm struggles with peaks, it is not a sales problem, it is a delivery system problem. A clear SOP for 8864 keeps reviewers out of loops and protects deadlines.

- SOP‑driven execution, the same steps for bookkeeping, tax, and 8864 attachments every time.

- Structured workpapers, standard file names, clean version control, and a summary index page.

- Multi‑layer review, preparer, senior, quality, then partner, with each layer checking a different thing.

- Turnaround SLAs, predictable windows for certificate requests and final review.

- Escalation control, issues flagged early to avoid eve‑of‑filing surprises.

- Continuity plans, zero disruption if someone is out.

If you want help implementing that structure inside your own systems, Accountably can integrate trained offshore teams through a delivery architecture built for speed, review efficiency, and accountability. We mention it briefly here because it solves the exact pain points you see with 8864, missing attachments, unclear ownership, and rushed workpapers.

Additional Resources And Related Articles

| Resource | Purpose | Notes |

| IRS Instructions for Form 8864 | Eligibility, timing, components | Check the version for your filing year |

| IRS, general business credits, Form 3800 | Passthrough reporting and ordering rules | Use the right line for each component |

| IRS, Form 8453 | Paper attachments when e‑file PDFs are not possible | Mail promptly and keep proof |

| ProConnect or Lacerte help | Where to enter and how to clear diagnostic #10568 | Attach PDFs or generate 8453 |

| TaxSlayer Pro knowledge base | 8864 location and 8453 steps | Follow current‑year guidance |

FAQs

What is Form 8864 used for

You use Form 8864 to claim section 40A biodiesel and renewable diesel credits and the section 40B sustainable aviation fuel credit. You compute each component separately, attach required certificates or statements, and carry the total to your return. Entities that generate the credit file 8864, owners who only receive passthrough amounts use Form 3800.

When do I claim the credit

Claim in the tax year the fuel is sold or used. Production or purchase dates do not control. For passthroughs, align to the entity’s sale‑or‑use year shown on the K‑1.

Do I need to attach documents

Yes. For biodiesel and renewable diesel, attach the Certificate for Biodiesel and, if applicable, the Statement of Biodiesel Reseller. For SAF, retain lifecycle analysis, certifications, and any required declarations. If you cannot e‑file PDFs, generate Form 8453 and mail support.

How do I clear diagnostic ref. #10568

Attach the missing biodiesel certificate or reseller statement as a PDF in your e‑file package, or check the option to generate Form 8453 and mail the documents. Re‑run diagnostics to confirm it is cleared.

Can I claim both excise and income tax credits on the same gallons

No. Reconcile Forms 720, 8849, and 4136 with 8864 so you do not double claim the same gallons. Use a reconciliation note in your workpapers so reviewers can sign off fast.

What changed for 2025

Always check the return year first. Many fuel incentives shift to a production‑based regime for 2025 activity with different forms, claimants, and documentation. If a client expected to file 8864 for 2025 sales, pause, review the law that applies to those gallons, and confirm the correct form and registration requirements.

Conclusion

You are the pilot of this return, and Form 8864 is your flight plan. Keep timing tied to sale or use, treat documentation like a non‑negotiable, and make your software steps boring on purpose. When you do, reviews are faster, partner time shifts to advisory, and deadlines stop feeling risky. If your team wants production stability without chaos, bring delivery structure to your 8864 process, and, when you are ready to scale that structure, consider a disciplined offshore layer that runs inside your systems with clear SOPs, SLAs, and layered review.

Simplify Delivery, Improve Margins, Stay in Control.

Offshore support that works exactly like your in-house team.

???? Let’s Talk